Financial Literacy Information

Throughout the world, finances seem to be an ongoing problem for most households. An alarming amount of people can’t produce $400 during an emergency situation, and although there are many reasons for this, it may be assumed that financial illiteracy is a root cause. Studies show that without a foundation in financial literacy, students cannot fulfill their ultimate financial potential. Happily, there is a plethora of financial literacy information out there, and financial education programs have bridged the gap, attempting to provide reliable information to willing parties everywhere.

Where To Find Information About Financial Literacy

If you’re looking for financial literacy information, keep in mind that different organizations and government agencies have their own definitions of the term. In general, “financial literacy” requires an understanding of how money works along with possession of the knowledge necessary to make healthy and sustainable financial decisions. Studies have shown that many individuals are financially illiterate and lack the knowledge foundation to make sound decisions. Financial education programs have stepped in to help ameliorate this dearth of financial literacy among individuals.

Factors Molding Financial Behavior

In a survey by OECD, well over a quarter of respondents replied that their culture influenced their attitudes toward wealth. https://www.oecd.org/finance/financial-education/2017%20Seminar%20on%20financial%20education

%20and%20financial%20consumer%20protection%20LAC%20Wood%20.pdf

An additional year of schooling increases the probability of having an investment income by 4.4% for whites and 1.7% for blacks. http://www.people.hbs.edu/scole/webfiles/cole-shastry-smarts%20HBS%20working%20paper.pdf

The Federal Deposit Corporation (FDIC) analyzed the intermediate-term impact of a financial literacy program on consumers’ behavior and confidence 6 – 12 months after the end of the program. They found that consumers were more likely to have a checking account, budget wisely, save for retirement, and more. After the program, 78% of respondents reported they had a checking account, up from 12% before they had undergone the program. Another 69% reported their level of savings had increased after taking the program, with only 3% reporting that it had declined. https://www.fdic.gov/consumers/consumer/moneysmart/pubs/ms070424.pdf

Researchers take advantage of a survey recording self-reported savings rates, as measured by amount of unspent take-home pay along with voluntary deferrals (e.g. 401(k) plan), and the state the respondent went to high school in. This is used to determine whether state mandated financial education curricula have an impact on the amount individuals save. Those entering high school five years after the implementation of the mandate had a savings rate of 1.5 percentage points higher than for students not exposed to a mandate. http://www.nber.org/papers/w6085.pdf

The Personal Impact of Access to Financial Illiteracy Information

Vermont, which ranked 2nd out of all 50 states on a financial literacy assessment, had the lowest rate of non-bank borrowing methods, at 15.2%.http://www.usfinancialcapability.org/downloads/NFCS_2015_State_Rankings.pdf

Less than one in ten (7%) understand that small company stock funds have a higher return over time than large company stock funds, dividend paying stock funds, or high yield bond funds. http://retirement.theamericancollege.edu/sites/retirement/files/2017_Retirement_Income_Literacy_Report.pdf

Households that scored higher on a specially constructed investment knowledge index were found to be more likely to have a diversified portfolio and have a 401(k) account. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

A study undertaken in the Dominican Republic compared two distinct approaches to financial literacy: a standard accounting curriculum and a rule-of-thumb training that taught financial heuristics. The simpler rule-of-thumb training was found to produce a larger effect in firms’ financial practices and made them more likely to keep accounting records, forecast monthly revenues, and objectively report financial figures. https://www.povertyactionlab.org/sites/default/files/research-paper/124_303%20Rules%20of%20Thumb%20AEJ%20Apr2014.pdf

The Current Financial Situation Facing Adults Today

Researchers asked individuals two sets of questions, one pertaining to basic financial literacy while the other related to advanced financial knowledge. The researchers then applied statistical techniques to construct indexes of financial knowledge. The probability of participating in the stock market increased 14 percentage points with a one standard deviation increase in advanced financial knowledge. In addition, a one standard deviation increase in basic financial literacy increases the probability of saving for retirement by 20 percentage points. https://www.dnb.nl/en/binaries/working%20paper%20313_tcm47-257145.pdf

46 percent of respondents said they either could not cover an emergency expense of $400 or would cover it by selling something or borrowing money. https://s3.amazonaws.com

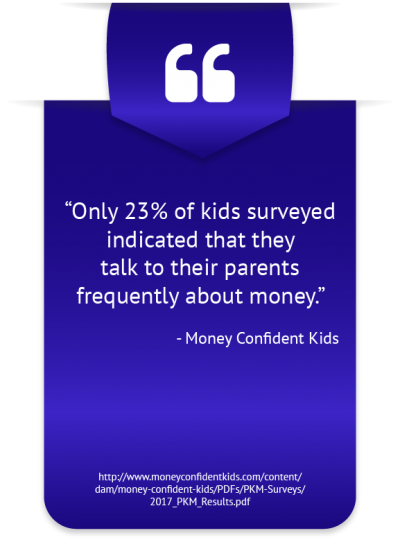

57% of millennials have either an advisor or robo advisor. http://www.moneyconfidentkids.com/content/dam/money-confident-kids/PDFs/PKM-Surveys/2017_PKM_Results.pdf

The Federal Reserve Board’s Division of Consumer and Community Affairs suggests that public service announcements could connect people to essential financial education material. Programs could partner with local newspapers to help elucidate the economic benefits of financial competency. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

The Growing Demand for Financial Literacy Information

The growing epidemic of individuals without a strong base in personal finance knowledge has prompted more and more to seek financial literacy information. The financial literacy information they receive is often of a lower quality than one might expect. The number of youth with considerable expertise in STEM fields but utterly lacking in basic financial competency is strikingly high. In order to raise a well-rounded generation of youth ready to tackle the financial challenges they will encounter, financial literacy programs and government policies promoting financial knowledge must be supported.