Financial Literacy Test Center: National Test & 33 Other Complimentary Tests Completed by Over 170,000 People

The NFEC’s Financial Literacy Test Center provides complimentary tests and testing results. Organizations and individuals are welcome to use this online evaluation material for pre-and post-testing, self-assessment, and/or to gain a better understanding about various financial literacy topics.

The Center was developed with three objectives: providing resources for financial educators, offering tools for people interested in improving their financial knowledge, and giving the media up-to-date information about the current state of financial education. The data gathered using these resources will be used to help adapt NFEC programs to accommodate different learner needs.

The NFEC’s financial literacy test results have been featured in Huffington Post, The Hill, Yahoo Finance, Business Insider, MarketWatch, Forbes, CNBC and many major media outlets. More than 170,000 people from all 50 states participated in our financial literacy tests and surveys.

Why is Measuring Financial Literacy Important?

The NFEC conducts multiple financial literacy tests and gathers survey data toward achieving that goal. Several government entities and financial services organizations also collect data on the status of financial literacy.

In this document, we compare some of those results in an attempt to paint a comprehensive picture of the financial literacy situation across the country. We update our statistics annually, and data from other sources as often as they are refreshed.

Select & Take the Test

Select Test to Participate In – All Complimentary

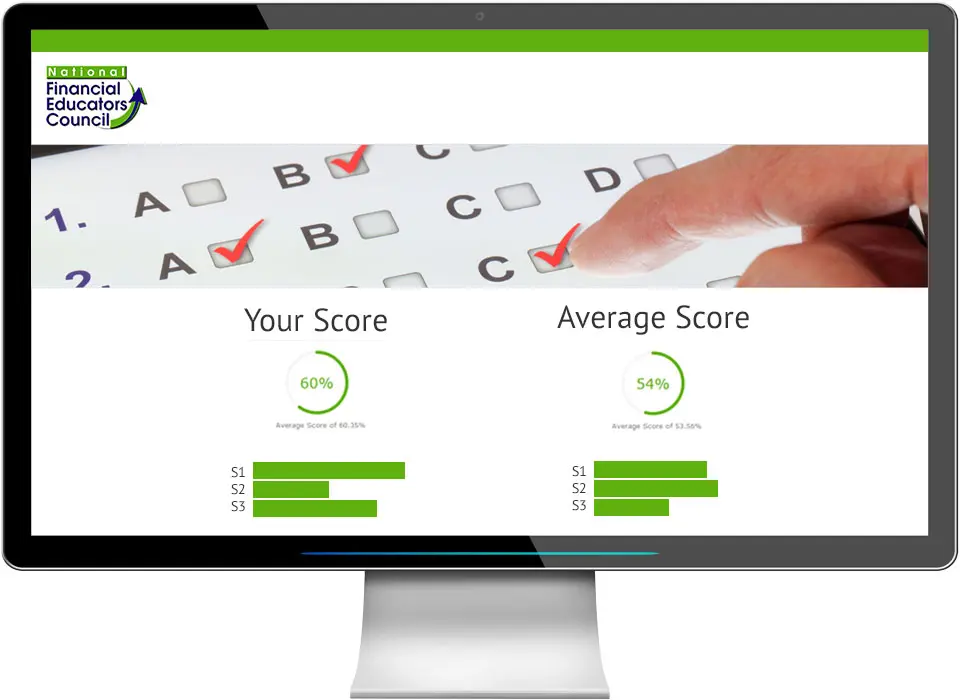

Receive Results

Receive Immediate Results & Compare with Others

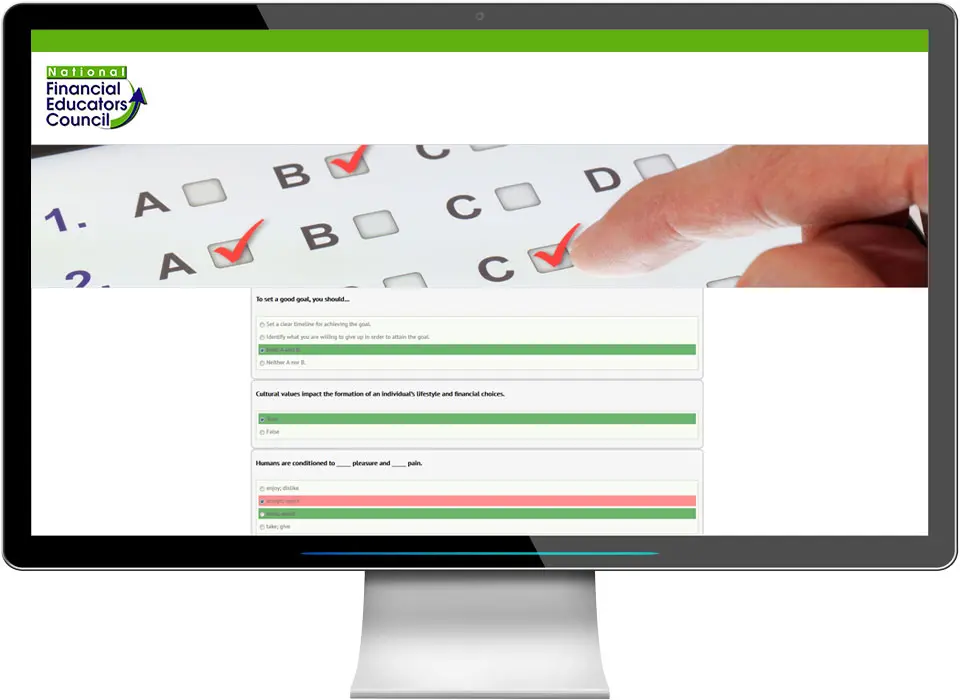

View & Learn

View the Questions, Correct Answers & Learn

Educators & Course Facilitators: Each student will receive results to them after they complete the test. To receive student results have them forward you their email.

*Tests and surveys provided may be used only on the NFEC website. Printing the tests or surveys is prohibited. Commercial use, sale, or any other use that violates the terms and conditions and copyright is prohibited.

Topic Based Tests

Average Score of the National Financial Literacy Test Segmented by Age

Over 100,000 people from all 50 states have completed the National Financial Literacy Test – a 30-question test designed to measure participants’ ability to earn, save, and grow their money. The test questions cover the 10 subjects covered in the Financial Literacy Framework & Standards and were written to measure 3 key areas: motivation to learn, subject knowledge, and recognition of the first step.

Although the National Financial Literacy Test was specifically designed for 15- to 18-year-olds, people of all ages have taken part in this assessment. See details below – for the latest national financial literacy test results click here.

10 – 14

Years of Age

Average Score of 56.72%

15 – 18

Years of Age

Average Score of 64.39%

19 – 24

Years of Age

Average Score of 70.87%

25 – 35

Years of Age

Average Score of 75.95%

36 – 50

Years of Age

Average Score of 76.94%

51+

Years of Age

Average Score of 77.85%

Financial Literacy Test Question Features

The NFEC’s financial education test measures each of the 10 areas covered within the financial literacy standards. These topics include: Financial Psychology, Credit & Debt, Accounts & Budgeting, Skill Growth, Income, Business Relations, Long-term Planning, Risk Management, Investments, and Social Enterprise.

The NFEC’s National Financial Literacy Test measures each of the aforementioned subjects and breaks the test down into three distinct areas that affect one’s financial capability.

Sample Question & Results:

How can understanding risk management topics help me in everyday life?

Sample Question & Results:

From the following list, choose the two best suggestions for building and maintaining a good credit rating.

Sample Question & Results:

How do I begin the process of creating a long-term financial plan?

Those Conducting Financial Education Programs are Encouraged to Measure Impact

The NFEC recognizes the importance of measuring all the elements that go into developing a successful financial literacy campaign. Measuring these three areas enables the design of a comprehensive financial education initiative that will maximize participant results.

Conducting financial literacy tests can help your organization evaluate your financial education program and its instructors and have a direct impact on your funding. Administering testing before and after your financial literacy program is an important part of developing a sustainable campaign.

The NFEC includes quizzes and tests with their entire financial literacy curriculum (free lesson plans) and events. In addition, the NFEC offers customized financial literacy testing, measurement, and long-term studies that measure changes in behavior.

With comprehensive pre- and post-testing, your organization stands a better chance of receiving financial literacy funding. This may help your organization sustain your programs and reach more people with the training. Gathering quantitative data can measure students’ understanding and the overall effectiveness of your financial education program. Learn more about the National Financial Educators Council’s tests that are included in our curriculum and financial literacy programs.

To learn more about the National Financial Educators Council’s financial literacy tests, complete the form located on the ‘Contact Us’ or ‘Solution Center’ page.

National Media Coverage of NFEC Testing & Surveys

Financial literacy gaps could be costing you more than you think. Asked to put a dollar figure on how much money they have lost in their lifetime due to personal finance missteps, nearly 25 percent of consumers estimated the cost at $30,000 or more, according to a new survey from the National Financial Educators Council. (The group polled 3,006 adults in mid-March.) More than a third put their losses at $999 or less.

Respondents Losing $30,000 or more; Sample Size

Over the course of a little over three years, the National Financial Educator’s Council administered a national financial literacy test to 4,916 youth between the ages of 15 and 18, from more than 40 states in the United States. The average score was 60.08 percent. In any standard “classroom” 60.08 percent would be a failing grade.

Participants from 40 States & Sample Size

A financial literacy test given by the National Financial Educator’s Council found that test-takers from 15-18 years old scored an average of only 59.6%. No matter what they’re learning in school, most young Americans are lost when it comes to managing their money.

National Financial Literacy Test Average Score & Sample Size

Despite their efficacy, a small portion of employers have been using pre-employment screenings. Only a quarter of job applicants said an employer checked their financial background and 5% were rejected from a job due to their financial profile, according to a survey of 1,165 U.S. workers by the National Financial Educators Council, a financial education company. [Employee Financial Wellness]

Survey Response & Sample Size

According to the results of a 2014 National Financial Educator’s Council’s survey, only 58 percent of America’s high school students passed a basic financial literacy test. The same study found that 96 percent of respondents would have made different decisions pertaining to their higher education if they were more aware of the repayment process.

Survey Accompanying the National Financial Literacy Test Score

29 Money Lessons Every High School Graduate Should Know. A financial literacy test given by the National Financial Educator’s Council found that test-takers from 15-18 years old scored an average of only 59.6%.

National Financial Literacy Test Average Score & Sample Size

You know your teens can be illogical, unreasonable, and occasionally malodorous, but isn’t it at least reasonable to assume they know the basics about money? Apparently not. Surveys [National Financial Educators Council] show that teens are failing at financial literacy. And while financial institutions like PricewaterhouseCoopers are investing significant resources in changing that, the problem is persisting.

The National Financial Educators Council (NFEC) released their report from the National Financial Literacy Test and the results were depressing. The NFEC surveyed 11,000 people from all 50 states and the average score from 15- to 18-year-olds was 60.35%.

National Financial Literacy Test Average Score & Sample Size

Trade Industry Coverage of NFEC Testing & Surveys

More than 51 percent of young adults across the United States say that a high school money management class would have benefitted their lives, according to a study from the National Financial Educators Council.

Data through February 2014 from the National Financial Educators Council’s (NFEC) National Financial Literacy Test, which tests youth between 15 and 18 on the areas covered within national financial literacy standards, reveals that: 115 (4.7%) participants achieved a score at or above 90%. 271 (11%) achieved a score at or above 80%. 539 (21.9%) achieved a score at or above 70%. 1,534 (62.4%) participants scored at or under 69.9%.

96% of adults agree that kids under 21 years old should be required to take a personal finance course. The National Financial Educators Council’s Financial Literacy Test – the average score was 60%.(/p>

While you may think this is an unlikely scenario, a recent survey by the National Financial Educators Council shows this is sadly a trend. It found that more than five percent of job hunters have been turned down from a position because of their financial situation.

The National Financial Educators Council found 19-24 year olds have low financial literacy. Fifty-one percent believe a personal finance class in high school would have helped them prepare for life. Whether there is a formal class or not, parents can help children understand that bills, budgets and payments recur every month—and the money has to come from somewhere.

“…the National Financial Educators Council (NFEC) have used surveys to collect information related to the level of understanding on financial topics. Surveys provide for anonymity as well as consistency as each respondent receives the same questions. Surveys allow for the acquisition of specific measurable data and comparison of that data across target populations. The results of a well-designed survey clearly answer a specific question. Surveys that answer the same question over a period of time also create opportunity to measure effectiveness of education.

Local News Coverage of NFEC Financial Literacy Tests & Surveys

AL.Com

A recent survey asked 1,100 young men and women ages 18 to 24 what high school courses would have benefited their lives most. Just over half – 51.4 percent – answered they think learning more about how to manage money would be more valuable to them than any of the other choices. The survey was co-sponsored by the National Financial Educators Council (NFEC), DreamCatcher Wealth Management, and The Minerva Foundation.

Fox 13

Surveys conducted by the National Financial Educators Council fond teaching money management in school has a big impact on students’ attitudes towards money and their budgeting behaviors later in life. And a new Bank of America USA Today survey shows just 30-percent of respondents thought their high school education did a good job teaching good financial habits.

Washington’s Top News

The National Financial Educators Council recently surveyed adults 35 to 54 years old about their experience in the hiring process. Among the 1,200 people who responded to the nationwide poll, 5.2 percent said they had been turned down for a job because of their financial profile. When asked if their employer ever conducted a credit of financial background check as a condition of being hired or getting a promotion, 26.3 percent said yes.

Savannah CEO

Another interesting finding was that, among people residing in urban areas, those who earned between $50,000 and $74,000 per year were more likely to choose “money management” as the most beneficial course than did those earning $25-49,000 annually. This research was sponsored by the collaborative efforts of the NFEC, DreamCatcher Wealth Management, and The Minerva Foundation for Financial Literacy.

Erin Mitchel, National Financial Educators Council Contributing Writer

As most of us are aware, money management skills are important for children to develop at a young age.

The effectiveness of this curriculum should be an ongoing process of education, implementation and monitoring how much participants retain by offering a series of financial literacy tests and financial literacy quizzes.

Hands on testing of practical matters can provide a student the experiential learning experience of the material they studied and will directly impact their short and long-term goals. The written section of within a financial literacy test helps them to identify the areas where more study is required.

Professional finance speakers understand effective administration of a financial literacy test it is important to conduct a pretest first. This will give you a base line of the student’s knowledge. If the delivery of the financial literacy curriculum and test is home be sure not to lead your student into answers during the pre and post test. Let them do the work on their own to get the most reliable data.

After the students have received some type of high school financial literacy curriculum the next step is to administer the post test. Ensure the post financial literacy test covers the material they learned and be sure not to skip portions of the financial literacy lesson plan that may be on the financial education test.

Financial literacy tests can include a wide variety of topics like: how to pick a career, comparing the pay between job offers, how to pay your bills on time, budgeting for living expenses, how to start saving for short term goals, comparing credit card offers, and a variety of other subjects. Be careful to choose financial education tests that align with the subjects you are teaching.

National Financial Educator’s Council (the NFEC) Real Money Experience (RMX) is a prime example of the practical teaching method that works with kids and has excellent results on post financial literacy test. The students visit twelve different stations, meet with financial literacy speakers and make life decisions that will impact them when they move away from home.

The experiential learning experience the students receive when they enter the RMX event will provide them hands on experience so the information is retained; thereby improving the results of the post financial literacy test.

The Real Money Experience event has students choosing a career and making education choices that affect their income. They decide on clothing and transportation options that fit their career while the financial literacy test is if their choices will fit into their budget.

Participants of this financial education event quickly become aware of the ongoing expense of each decision. The expenses can be as simple as insurance, dry cleaning or utility costs, for example. The volunteers help participants set up a saving plan that matches their future lifestyle goals, create a budget, make credit and investment decisions and this interaction acts as a financial literacy quiz as students enter each booth.

The end of the financial literacy class is capped with a practical financial literacy test based on the lessons they learned.

Establish clear, quantifiable goals for your financial literacy program. Then develop financial literacy testing that measures your specific objectives. Organizations commonly use generic pre- and post-testing instruments that may fail to accurately measure the results of their specific programs. As an example of good measurement, view the survey and testing results from a recent half-day financial literacy program with the Simon Family Foundation.

Click below to view the report:

Final Report – Simon Family Foundation 2012

The National Financial Educators Council (NFEC) was honored to serve the Simon Family Foundations’ annual Summer Conference. The NFEC commends their efforts to provide their ‘Scholar’ mentoring, support and training that will help them in college and beyond.

The generous scholarships offered to each Simon Scholar is commendable and contributes to maintaining a 90% success rate of students active in the program or graduated from college. The NFEC believes through these various programs they will enter college with enhanced self-confidence and self-esteem which helps them earn their degree and maximize the college experience.

2011 Summer Conference – Real Money Experience Money Management Workshop

The Simon Family Foundation hosts several events throughout the year to facilitate interaction between the students and provide them intensive, yet fun, training sessions. The main event held eanoch year is the Summer Conference .

The 2011 Summer Conference was hosted at Chapman University and had over 120 current Scholars and alumni participating in this three-day money management workshop. Students participated in a variety of activities designed to prepare them for the ‘real world’.

One of the many highlights of this conference was the National Financial Educators Councils’ hands on money management workshop, the Real Money Experience. Simon Scholars visited twelve separate booths and made life decisions that will impact them when they move away from home.

According to research conducted in 2012-13 by the National Financial Educators Council (NFEC), an overwhelming majority (96%) of U.S. adults who completed an online survey said they believed college students should be required to take a financial education course before entering into student loan debt. At the same time, the NFEC also conducted a financial literacy test with more than 1,300 American youth aged 15-18; the results of that study indicated that less than one-third of teens were able to score at the 70th percentile or better.

The NFEC is the go-to source in the industry for evidence-based surveys and tools to assess financial knowledge and measure the success of financial education campaigns. A for-profit financial education council with a social enterprise business model, the NFEC created its financial literacy assessment test to help illuminate key money management topics around which the country’s young people need to improve their skill sets. Whether or not to take on student loan debt represents one of the essential decisions facing teens today as they prepare for college. Teaching money management skills may be the single best way to help young adults get ready to become successful, productive members of society.

Between January 2012 and August 2013, youth across America were invited to complete a web-based financial knowledge test that measured respondents’ current levels of understanding about key personal finance concepts. The purpose of the study was to quantify the financial capabilities of teens and young adults and to illuminate the topic areas where young people may need more education. Among the 1,309 young people (aged 15-18) who completed the test, 952 (72.7%) were unable to answer 70% correctly. The average score across the sample was 58%.

In a separate study conducted near the same time frame, the NFEC surveyed 452 U.S. adults regarding their opinions about important financial literacy topics. In addition to finding that most adults support financial education before entering into a student loan, this analysis discovered that 93% of respondents believed the fact that students do not understand the consequences of student loans was a “very big” or a “big” problem. These findings point to a serious need for financial education programs aimed at college students. The NFEC has answered this call by designing state-of-the-art college financial literacy curriculum packages.

Taking a personal financial literacy test will highlight the strengths and weaknesses in your financial knowledge. Choose to test yourself on any aspect of personal finance. We send the results via email, so you can review your answers while the material is still fresh in your mind. You can then focus on your weaknesses and build up your arsenal of financial knowledge. Who knows what that will be worth in the coming years.

Financial literacy is more than book knowledge

Yes, it important to track book knowledge, but it’s not the only aspect of money management that a personal financial literacy test should measure. Not addressing any one of these angles causes a possible point of implosion for your entire financial education program. Unconscious ill feelings toward money will probably lead to detrimental, self-destructive behavior with money. Exposing either of these warning signs of failure is critical to success.

Who should use a financial literacy test? Financial educators, financial coaches and financial service professionals should all know the competencies of their participants. Ellis Cropper, founding member of the Massachusetts Financial Educators Council, noted the results across the state were about average compared to other areas of the country, but people lacked the confidence in making financial decisions.

We also track and measure students’ ability to incorporate what they’ve learned into their own lives. Students create and (ideally) implement their own financial systems. Ultimate success can be seen only in a student’s personal financial situation before and after the course.

Stay aligned with the student’s needs by measuring depth of knowledge

When students don’t progress at the rate intended by the course, they get frustrated and stop learning. It usually shows a disconnect between how the information is being presented and the students. In other words, the students might not be able to relate to the information, how it’s being presented or who is presenting the material. It takes more than knowing the financial literacy definition – it takes molding positive behaviors.

To make sure the students are progressing in harmony with the course presentation, we measure the depth of understanding throughout the course. Based on Webb’s Depth of Knowledge and Bloom’s Taxonomy of Thinking Skills, we design our personal financial literacy tests to gauge the students’ level of understanding and make sure it is aligned with the course timeline progression. This is far more involved than just reading a personal financial literacy test pdf.

When planning a personal finance educational event, it’s crucial to ensure that the event meets the unique needs of its target audience. Perhaps the single best way to do that is to go straight to the horse’s mouth. In other words, involve the participants in the planning process. The National Financial Educators Council has financial literacy tests that can help during the early stages of planning, as well as after the event when you seek to measure program impact.

You probably are starting with a good idea about who you want to reach and what type of event you’d like to present. But before you even begin planning, conduct good research to test your program concept. Such research might involve a financial literacy assessment among potential attendees at the event, to point out areas where they most desire education and characterize their learning capabilities.

First, talk with your network of friends, colleagues, and community members who work with your target audience. Gather ideas about the needs of the participants and the best ways to reach them. Then reach out to the participants themselves. The NFEC can provide a sample financial literacy test that examines participant knowledge. Also conduct outreach via surveys and informal face-to-face interviews. Collecting information about what people are most motivated to learn and teaching methods they prefer will help you design a program that meets, or even exceeds, participant expectations.

Another important piece of planning is preparing a personal finance quiz that measures what participants know about money management both before and after they attend the event. If you can demonstrate that people learn key money skills, you’ll be better able to build support for future initiatives. Make sure the quiz measures the same skills you’re presenting in the educational materials—that is, “teach to the test.”

The NFEC financial literacy tests and approach to teaching financial literacy is holistic, meaning they have fully imagined the process from start to finish. They place heavy emphasis on measurement because that’s how programs meet participant expectations and promote long-term behavior change.

You may be also interested in these financial education tests & surveys:

Parenting & Financial Education Survey

*Tests and surveys provided may be used only on the NFEC website. Printing the tests or surveys is prohibited. Commercial use, sale, or any other use that violates the terms and conditions and copyright is prohibited. Read complete terms and conditions of use.

In these trying financial times it has never been more important that our country’s youth gain practical money management skills. The National Financial Educators Council (NFEC) has recognized this need and this organization has positioned itself as an esteemed leader in providing successful financial literacy promotions. One essential component of such an initiative, according to the NFEC, is evaluation. Every youth financial educational program should be accompanied by a high school financial literacy test to examine students’ knowledge base, both before and after they receive the education.

There are several reasons to conduct a financial literacy exam as a pre- and post-test measure. First and foremost, testing will evaluate program effect. How much did the students learn? How motivated have they become to learn more about money? And do they recognize the first steps they should take toward positive action to secure their financial futures?

Second, if a program is proven to be effective, the financial literacy test can open up opportunities to garner funding. Potential sponsors want to know a program works before they decide to back it. Positive results on the test shows funding agencies that the education makes a difference. And gaining funds helps ensure that the program can be sustained into the future.

Third, a high school financial literacy test helps point up areas for improvement. For example, if student results on the financial literacy quiz demonstrate high knowledge levels about budgeting but lower marks in credit and debt, that result may indicate that more emphasis on credit and debt topics would make the program better.

Finally, accurate measures help demonstrate the long-term effects of personal finance lesson plans on behavior change. The NFEC suggests that behavioral measures should be used for comprehensive financial literacy training programs. For instance, a program that educates kids about the value of savings might follow up one year later to find out how much participants’ savings accounts balances have increased since the training.