Financial Literacy Facts

While it may be general knowledge that the youth of today are not financially literate, this vague awareness is doing nothing to encourage educational institutions to either start new programs or improve those already in existence. However, by collecting and distributing facts about financial literacy, advocates can begin to encourage more support behind financial literacy programs. Research that demonstrates the exact financial weakness of the population and research showing financial literacy facts on programs that successfully make a positive impact helps educators determine the needs of their students for new programs and enhance aspects of existing programs.

The Function of Financial Literacy Facts

Facts about financial literacy paint a vivid image of financial competency among different groups of the population. A plethora of research papers and reports have yielded facts that illustrate the dismal state of financial knowledge among the public—especially among women, minorities, and other groups that would benefit economically from improved financial literacy. Financial literacy facts are used to both raise awareness about financial literacy and also help construct targeted curriculum that covers the financial needs of program participants.

Information Currently Molding Financial Behaviors of the Public

46% of those with low financial literacy index scores reported learning from personal experience, while 73% of those with high literacy scores claimed to learn from personal experience. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

40.2% of those with low levels of financial literacy relied on parents, friends, and acquaintances as their most important source of financial knowledge, compared to 20.8% of those with the highest levels of financial literacy. http://www.nber.org/papers/w13565.pdf

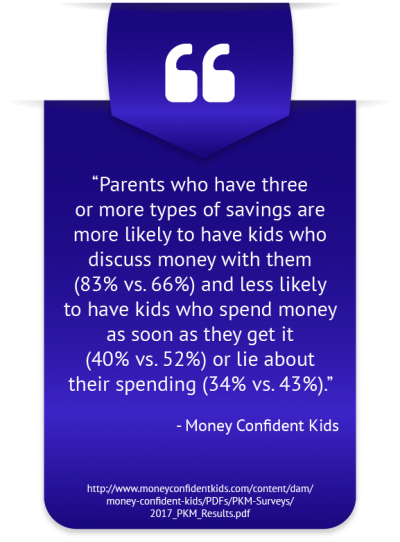

57% of millennials have either an advisor or robo advisor. http://www.moneyconfidentkids.com/content/dam/money-confident-kids/PDFs/PKM-Surveys/2017_PKM_Results.pdf

Personal Impacts of Financial Illiteracy

Borrowers who scored lowest on financial literacy tests were in mortgage delinquency 25% of the time, compared to the 12% mortgage delinquency for those who scored highest on the assessment. https://www.frbatlanta.org/-/media/documents/research/publications/wp/2010/wp1010.pdf

Households that scored higher on a specially constructed savings index were found to be more likely to own a checking account and have an emergency fund. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

North Dakota, which ranked 4th out of all 50 states on a financial literacy assessment, had the highest percentage of respondents at 55.5% declare they had an emergency fund. http://www.usfinancialcapability.org/downloads/NFCS_2015_State_Rankings.pdf

Pregnant or parenting teens are more concerned about learning to save for a home in the future than learning how to save for college. https://youth.gov/youth-topics/financial-capability-literacy/facts#_ftn8

Positive Effects of Financial Literacy

The Federal Deposit Corporation (FDIC) analyzed the intermediate-term impact of a financial literacy program on consumers’ behavior and confidence 6 to 12 months after the end of the program. They found that consumers were more likely to have a checking account, budget wisely, save for retirement, and more. After the program, 78% of respondents reported they had a checking account, up from 12% before they had undergone the program. Another 69% reported their level of savings had increased after taking the program, with only 3% reporting that it had declined. https://www.fdic.gov/consumers/consumer/moneysmart/pubs/ms070424.pdf

Attending a employer-sponsored retirement seminar saw net worth increase by nearly 27% for those who were in the lowest income bracket and had not received a high school diploma. http://www.dartmouth.edu

The State Bank of Pakistan and management consulting firm BearingPoint have partnered to develop the country’s first-ever nationwide financial literacy program. Products and services tailored for low-income Pakistanis will be developed to assist individuals in making financially sound decisions.

http://www.sbp.org.pk/press/2012/FinancialLiteracyProgram-20-Jan-12.pdf

Champlain College’s center for financial literacy emphasizes that financial literacy topics must be taught in a course that students are required to take in order to graduate. https://financialliteracy.champlain.edu/research-advocacy/2023-report-card-introduction/keys-to-success/

To Encourage Change, Facts About Financial Literacy Are Vital

While it is easy to feel discouraged after analyzing financial literacy facts, we must not believe that financial literacy for all individuals is too daunting of a task. The same reports and academic papers that produce such dismaying financial literacy statistics also affirm the promises of smart financial education programs. Financial education programs based on best practices have been shown to imbue learners with the knowledge they need in order to enact real changes in their financial behaviors.