Annual Survey Underscores the Persistent Cost of Financial Illiteracy in the U.S.

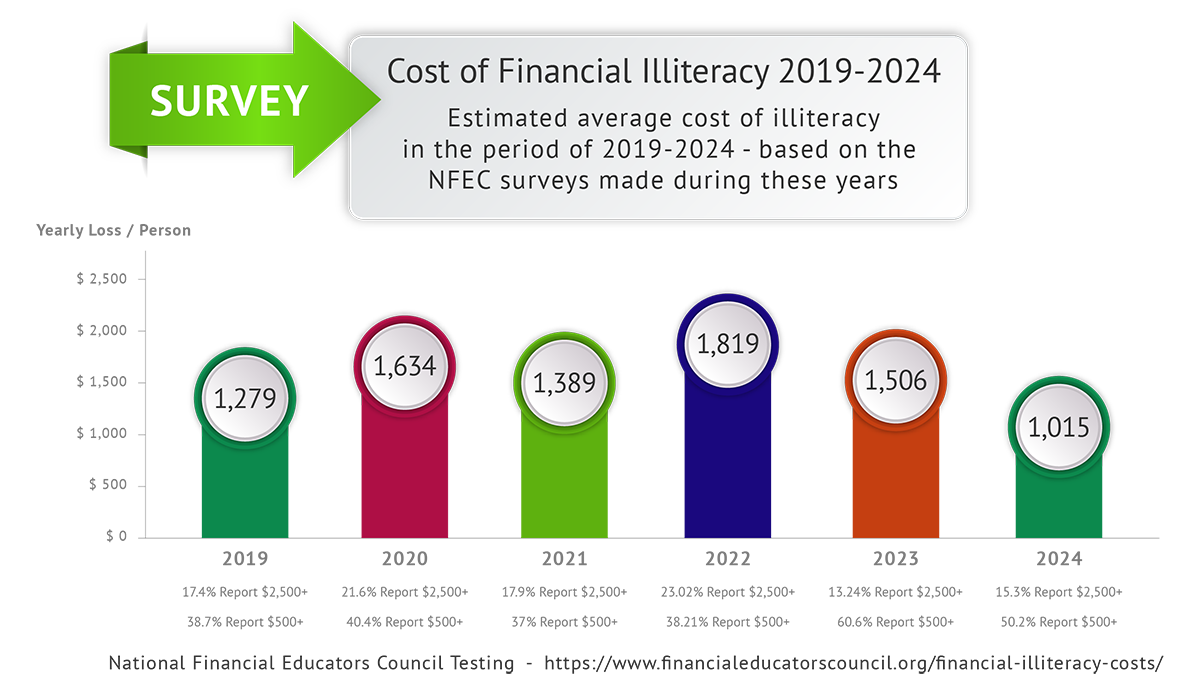

Each year, the National Financial Educators Council (NFEC) surveys American adults to estimate how much money they believe they lost due to a lack of personal finance knowledge. Across multiple survey waves, respondents have reported annual losses ranging from $948 to $1,819 – highlighting the substantial financial consequences tied to low financial literacy.

When these findings are extrapolated to the U.S. adult population (estimated at 260 million in 2025), the national cost of financial illiteracy reaches into the hundreds of billions of dollars annually.

2025 Financial Illiteracy Cost Results

The NFEC conducted a survey asking American adults to estimate how much money they had lost during the year due to lack of financial knowledge. The single-question survey asked U.S. residents across the country, “During the past year (2025), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 1,200 people responded to the survey between December 24 and December 28, 2025. Among this diverse group of respondents, the estimated average amount of money that lacking knowledge about personal finances cost people was $948 in 2025.

If we generalize the results to represent all of the approximately 260 million adults who live in the U.S., lack of financial literacy cost Americans a total of more than $246 billion in 2025.

2025 Survey Data

The survey asked 1,200 people across six age groups the following question:

During the past year (2025), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 –

$499

51.42%

$500 –

$999

16.33%

$1,000 – $2,499

17.67%

$2,500 – $9,999

10.25%

$10,000

+

4.33%

Additional Data

14.6% Report 2025 Losses at $2,500+

48.6% Report 2025 Losses at $500+

Survey Methodology: Data was collected by Prodege, a leading consumer insights firm, via the Pollfish platform using targeted demographic criteria and real-time sampling across mobile apps and websites. Prodege ensures data quality through AI-driven screening and a rigorous validation process, supporting high standards of accuracy and reliability.

The average respondent lost $948 due to lack of financial knowledge in 2025.

Past Survey Results, 2024 Data

The survey asked 1,200 people across six age groups the following question:

During the past year (2024), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 –

$499

49.83%

$500 –

$999

18.0%

$1,000 – $2,499

16.92%

$2,500 – $9,999

10.25%

$10,000

+

5.0%

Additional Data

15.3% Report 2024 Losses at $2,500+

50.2% Report 2024 Losses at $500+

The average respondent lost $1,015 due to lack of financial knowledge in 2024.

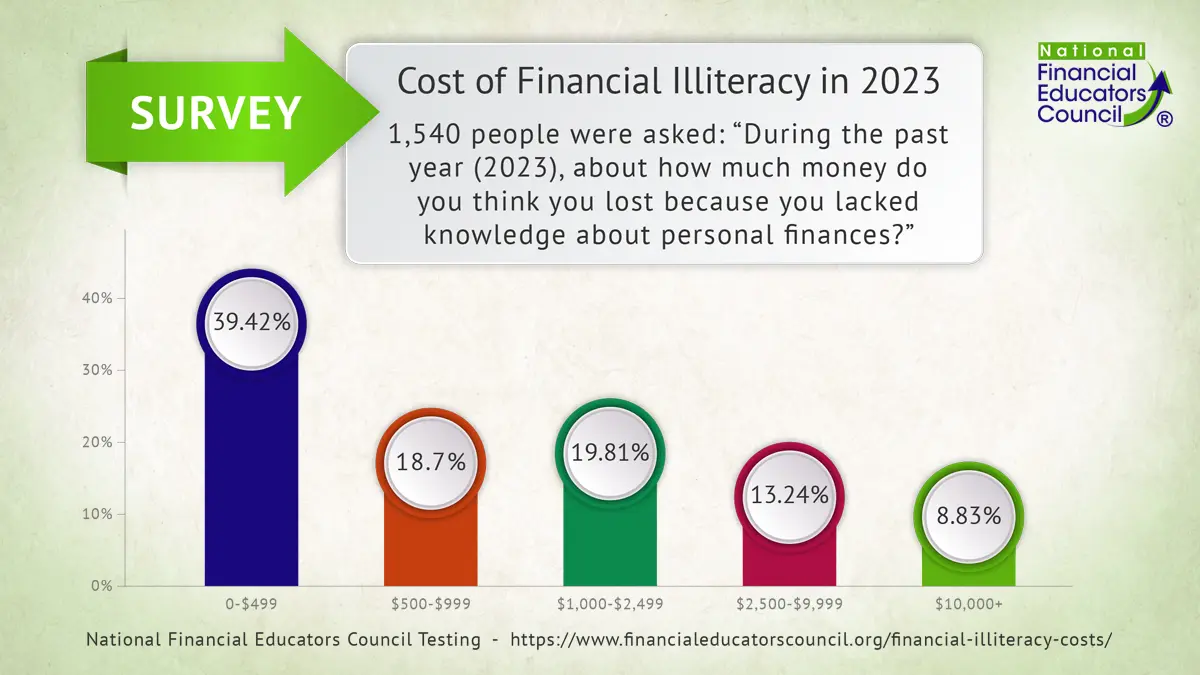

Past Survey Results, 2023 Data

The survey asked 1,540 people across six age groups the following question:

During the past year (2023), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 –

$499

39.42%

$500 –

$999

18.7%

$1,000 – $2,499

19.81%

$2,500 – $9,999

13.24%

$10,000

+

8.83%

Additional Data

22.07% Report 2023 Losses at $2,500+

60.58% Report 2023 Losses at $500+

The average respondent lost $1,506 due to lack of financial knowledge in 2023.

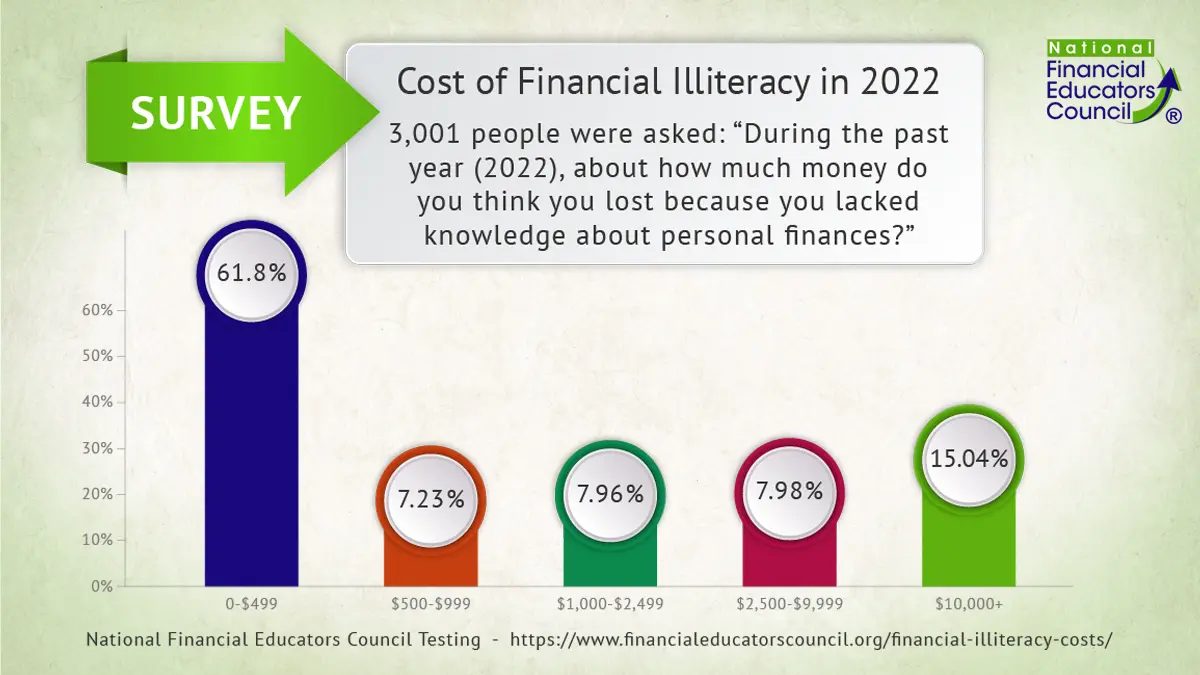

Past Survey Results, 2022 Data

The survey asked 3,001 people across six age groups the following question:

During the past year (2022), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 –

$499

61.8%

$500 –

$999

7.23%

$1,000 – $2,499

7.96%

$2,500 – $9,999

7.98%

$10,000

+

15.04%

Additional Data

23.02% Report 2022 Losses at $2,500+

38.21% Report 2022 Losses at $500+

The average respondent lost $1,819 due to lack of financial knowledge in 2022.

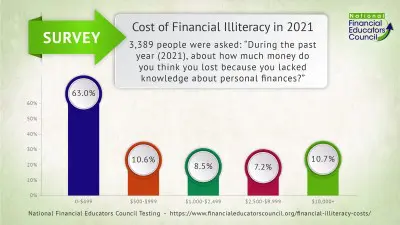

Past Survey Results, 2021 Data

Lacking financial literacy and not knowing how to manage one’s personal finances carried a high cost in 2021. The NFEC conducted a survey asking American adults to estimate how much money they had lost during the year due to lack of financial knowledge. The single-question survey asked U.S. residents across the country, “During the past year (2021), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 3,389 people responded to the survey between November 23rd, 2021 and December 23rd, 2021. Six different age groups across the U.S. were represented among those surveyed. Among this diverse group of respondents, the estimated average amount of money that lacking knowledge about personal finances cost people was $1,389 in 2021.

If we generalize the results to represent the approximate adult pupulation of the U.S., lack of financial literacy cost Americans a total of more than $352 billion in 2021.

The survey asked 3,389 people across six age groups the following question:

During the past year (2021), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 – $499

63%

$500 – $999

10.6%

$1,000 – $2,499

8.5%

$2,500 – $9,999

7.2%

$10,000 +

10.7%

Additional Data

17.9% Report 2021 Losses at $2,500+

37% Report 2021 Losses at $500+

The average respondent lost $1,389 due to lack of financial knowledge in 2021.

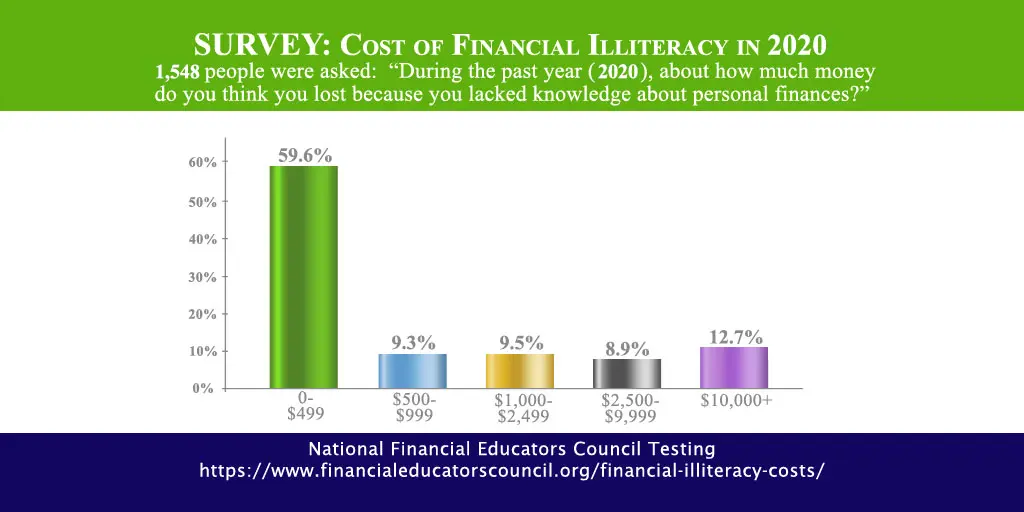

Past Survey Results, 2020 Data

Lacking financial literacy and not knowing how to manage one’s personal finances carried a high cost in 2020. The NFEC conducted a survey asking American adults to estimate how much money they had lost during the year due to lack of financial knowledge. The single-question survey asked U.S. residents across the country, “During the past year (2020), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 1,548 people responded to the survey between December 31st, 2020 and January 3rd, 2021. Six different age groups across the U.S. were represented among those surveyed. Among this diverse group of respondents, the estimated average amount of money that lacking knowledge about personal finances cost people was $1,634 in 2020.

If we generalize the results to represent the approximate adult pupulation of the U.S., lack of financial literacy cost Americans a total of more than $415 billion in 2020.

The survey asked 1,548 people across six age groups the following question:

During the past year (2020), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 – $499

59.6%

$500 – $999

9.3%

$1,000 – $2,499

9.5%

$2,500 – $9,999

8.9%

$10,000 +

12.7%

Additional Data

21.6% Report 2020 Loses at $2,500+

40.4% Report 2020 Loses at $500+

The average respondent lost $1,634 due to lack of financial knowledge in 2020.

Past Survey Results, 2019 Data

Lacking financial literacy and not knowing how to manage one’s personal finances carried a high cost in 2019. The NFEC conducted a survey asking American adults to estimate how much money they had lost during the year due to lack of financial knowledge. The single-question survey asked U.S. residents across the country, “During the past year (2019), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 2,506 people responded to the survey between December 31st 2019 and January 3rd 2020. Six different age groups across the U.S. were represented among those surveyed. Among this diverse group of respondents, the estimated average amount of money that lacking knowledge about personal finances cost people was $1,279 in 2019.

The survey asked 2,506 people across six age groups the following question:

During the past year (2019), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 – $499

61.33%

$500 – $999

10.53%

$1,000 – $2,499

10.73%

$2,500 – $9,999

7.30%

$10,000 +

10.09%

Additional Data

17.4% Report 2019 Loses at $2,500+

38.7% Report 2019 Loses at $500+

The average respondent lost $1,279 due to lack of financial knowledge in 2019.

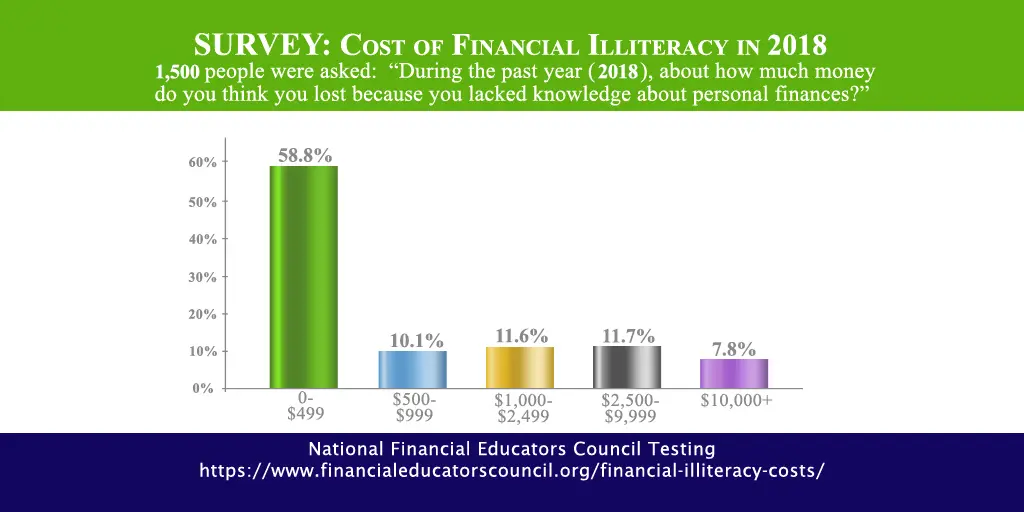

Past Survey Results, 2018 Data

Lacking financial literacy and not knowing how to manage one’s personal finances carried a high cost in 2018. The National Financial Educators Council (NFEC) sought to find out how much money people estimated they had lost across the year due to a lack of financial knowledge. In a one-question online survey, U.S. residents were asked, “During the past year (2018), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 1,500 participated in the survey between January 1st and January 4th, 2019, representing six age groups across the country. Among this diverse group, respondents estimated that lacking knowledge about personal finances cost them an average of $1,230 in 2018. This figure was calculated by averaging the total number of respondents selecting each category, using the lowest number in each spread.

The survey asked 1,500 people across six age groups the following question:

During the past year (2018), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices and Results Were:

$0 – $499

58.8%

$500 – $999

10.1%

$1,000 – $2,499

11.6%

$2,500 – $9,999

11.7%

$10,000 +

7.8%

Additional Data

19.5% Report 2018 Loses at $2,500+

41.2% Report 2018 Loses at $500+

The average respondent lost $1,230 due to lack of financial knowledge in 2018.

Past Survey Results (2017 Data)

This is the 2nd survey conducted by the NFEC that sought to find out how much money people estimated they had lost across the year due to a lack of financial knowledge. In a one-question online survey, U.S. residents were asked, “During the past year (2017), about how much money do you think you lost because you lacked knowledge about personal finances?”

A total of 1,515 participated in the survey, representing six age groups across the country. Among this diverse group, respondents estimated that lacking knowledge about personal finances cost them an average of $1,171 in 2017. This figure was calculated by averaging the total number of respondents selecting each category, using the lowest number in each spread.

The survey asked 1,515 people across six age groups the following question:

During the past year (2017), about how much money do you think you lost because you lacked knowledge about personal finances?

Available Choices Were:

The Results

18% Report 2017 Loses at $2,500+

41.2% Report 2017 Loses at $500+

The average respondent lost $1,170.95 due to lack of financial knowledge in 2017 alone.

Past Survey Results (March 2017)

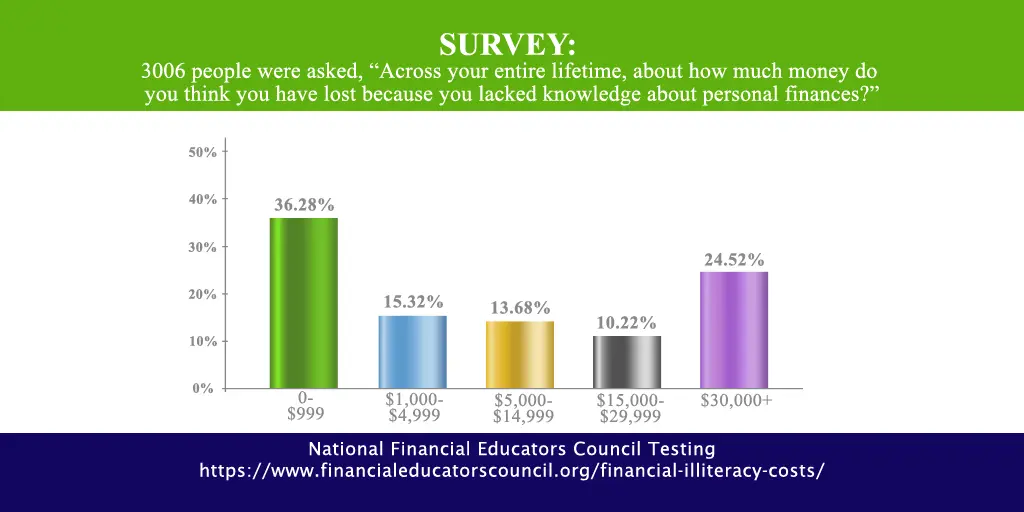

Between March 12th and 17th 2017, the National Financial Educators Council asked 3,006 across the US, “Across your entire lifetime, about how much money do you think you have lost because you lacked knowledge about personal finances?”

The survey was conducted online, answers were randomized and inferred demographic data was used. Respondents from 6 age groups (18 – 24, 25 – 34, 35 – 44, 45 – 54, 55 – 64, 65+) participated. The goal of the survey was to measure people’s opinions about the value of personal finance education relative to other coursework commonly offered by high schools.

The survey asked 3,006 people across six age groups the following question:

Across your entire lifetime, about how much money do you think you have lost because you lacked knowledge about personal finances?

Available Choices Were:

The Results

Reported lifetime losses over $15,000 were reported by 1 out of 3 respondents.

1 in 4 people reported losses over $30,000 due to a lack of financial knowledge.

Using the low end of the numeric spread respondents lost $9,724.83 due to lack of financial knowledge.

Using the highest numeric spread ($30,000 was used for $30,000+ answer), respondents lost $13,237.94.