Financial Illiteracy: Research, Data, Definition, & Opinions

Americans and other societies throughout the world share a common problem – financial illiteracy is pervasive in cultures around the globe. This epidemic threatens to undermine people’s lives. Not only does bad financial planning affect individual lives, but it often proves responsible for eating away at family cohesion.

It is extremely important to know how to deal with your personal finances prudently. Making the wrong decisions can lead to circumstances from which people might never recover. These problems can be prevented with just a little financial literacy put into practice. Even a small amount of knowledge can lead to more practical financial planning, which can make people’s lives more stable and comfortable.

Financial Illiteracy – What Exactly Is It?

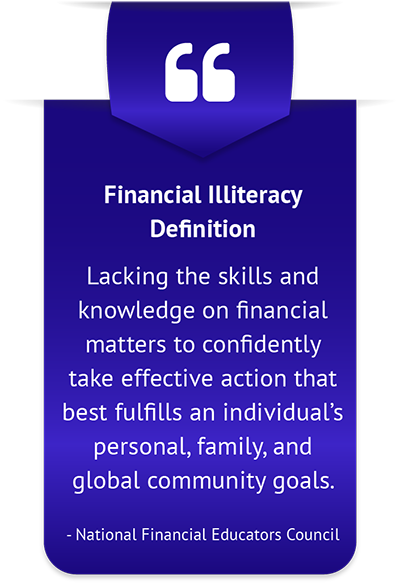

According to the National Financial Educators Council, financial illiteracy is “Lacking the skills and knowledge on financial matters to confidently take effective action that best fulfills an individual’s personal, family, and global community goals.” See other financial literacy definitions.

A person who is financially illiterate may inadequately save for retirement, spend more than their budget allows, and make other financial decisions that provide short-term gratification but result in negative long-term consequences. However, there may be other causes beyond just financial illiteracy that affect a person’s financial situation. Financial problems can occur due to unfortunate behaviors, past mistakes, and even lack of opportunity – all these issues can have an impact equal to or greater than financial illiteracy.

People are Ashamed of Being Financially Illiterate

44% of Americans aged 22-26 do their own taxes (Bank of America). https://bankofamerica.com

85% claimed they were ‘somewhat’ or ‘very’ unlikely to discuss their amount of credit card debt with strangers, more than the percentage of respondents who would avoid divulging details about their love life (CreditCards.com). https://www.creditcards.com/credit-card-news/poll-credit-card-taboo-subject-2013-1276.php

26% of adults admit to not paying their bills on time (National Foundation for Credit Counseling). https://www.nfcc.org

46 percent of respondents said they either could not cover an emergency expense of $400 or would cover it by selling something or borrowing money (ConsumerFinance.gov). https://s3.amazonaws.com

Financial Illiteracy Statistics

See the latest financial illiteracy cost data.

Targeted Technological Learning Can Improve Financial Literacy

The overarching purpose of financial education is not to transfer knowledge from educator to learner. Rather, the end goal of financial literacy initiatives is to elicit positive financial behavioral change by equipping program participants with the critical thinking framework they need to properly assess financial decisions in their lives.

Plenty of research papers have corroborated that financial literacy, when properly administered by a qualified financial educator, has the ability to make real improvements in the financial health of learners.

The Federal Reserve bank of Philadelphia found that counseling delivered via technology was actually better at molding consumer behavior than face-to-face counseling. Programs that are limited on funds can use technology as a means to reach more people with the same level of efficacy and with lower expenses (Federal Reserve Bank of Philadelphia).

https://www.phil.frb.org

57% of millennials have either an advisor or robo advisor (MoneyConfidentKids.com). https://www.moneyconfidentkids.com

What the Experts Say About Financial Illiteracy

“I think people don’t understand compound interest because typically no one ever explains it to them and the level of financial literacy in the US is very low.” – James Surowiecki, journalist at The New Yorker and author of “The Financial Page” column

“Without financial literacy, divorce rates soar, families rupture, and women stay with abusive men for financial security. A lack of jobs contributes to riots and illegal activity. Name any situation and it goes back to money. We need to focus on poverty eradication.” – John Hope Bryant, CEO of Operation HOPE

“The good news, though, is that all of us can improve the security of our futures through financial literacy. With a better understanding of the basics of finance—how to save, budget and invest—we can increase both our earning potential and our prospects for a solid financial future.” – Reba Dominski, President of U.S. Bank Foundation

The Dominican Republic says that financial literacy initiatives can simplify financial conceptions to help participants translate their knowledge into real world behavioral change. In addition, as evidenced by the difference between the effect of the two programs on firms and for entrepreneurs, the authors note that programs should be tailored based on the target audience to maximize potency (Poverty Action Lab). https://www.povertyactionlab.org

40.2% of those with low levels of financial literacy relied on parents, friends, and acquaintances as their most important source of financial knowledge, compared to 20.8% of those with the highest levels of financial literacy (National Bureau of Economic Research).

https://www.nber.org/system/files/working_papers/w13565/w13565.pdf

A mere 31% of young Americans thought that their high school education adequately taught them good financial habits(Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

Financial Illiteracy Statistics Demonstrate the Devastating Consequences

Financial illiteracy has become a point of concern for communities and governments worried about the effects such a critical lack of knowledge can have on the lives of individuals. Limited access to financial literacy classes and education leave people woefully unprepared. Equipped with only a partial and inadequate framework for thinking about financial decisions, too many individuals submit to making poor financial choices with long-term consequences that are difficult – if not impossible – to correct. Preventing and mitigating financial illiteracy requires the continued efforts of employers, governments, and the financial education industry.

[1] National Financial Educators Council, “Financial Illiteracy in America“

Research, Statistics & Quotes

NFEC Position Statement

People are going through financial hardships. From kids who lack basic necessities, to families seeing their dreams of retirement slip away – the financial challenges people face today have powerful impact on their health, well-being, and security. The epidemic of financial problems is vast.

It is the NFEC’s mission to provide tools, training, and resources to those who teach personal finance and advocate for increased access to financial literacy education. We honor our financial education champions and partner with them to spur this vitally important movement forward. No matter the size and scope of a program, our goal is to help it expand, improve results, and scale, so the effort can reach more people with this much-needed information.

Financial Illiteracy

Americans and other societies throughout the world have a share problem – financial illiteracy is pervasive in cultures around the globe. This epidemic threatens to undermine people’s lives. Not only does bad financial planning undermine individual lives, it is often responsible for eating away at familial cohesion

It is extremely important to know how to deal with your personal finances in a prudent manner. Making the wrong decisions can lead to circumstances from which people might never recover. These things can be prevented with a little financial literacy put into practice. A little knowledge can lead to prudent financial planning, which can lead to a stable, comfortable life.

Financial Illiteracy is a Worldwide Debilitating Condition.

Financial illiteracy is the lack of an ability to efficiently handle personal finance matters involving budgeting, saving, investing, and more. Surveys run by government agencies and financial education programs expose the lack of financial knowledge among both Americans and individuals globally. Financial competency is a basic requirement to lead a healthy financial life. Individuals afflicted by financial illiteracy are simply not able to discern between different financial choices and are often unable to reach their financial goals.

Need for Money Management Knowledge Growing, According to Financial Illiteracy Statistics

According to the American Dream Education Campaign, most students aged 15-21 report feeling unprepared to navigate today’s complex financial landscape. This finding is just one of the compelling financial literacy statistics that have driven the National Financial Educators Council into action. The NFEC, an independent financial education group with a social enterprise model, takes a holistic approach to promoting financial literacy – an approach which rests on the foundation of empirical research using rigorous methodologies.

According to the American Dream Education Campaign, most students aged 15-21 report feeling unprepared to navigate today’s complex financial landscape. This finding is just one of the compelling financial literacy statistics that have driven the National Financial Educators Council into action. The NFEC, an independent financial education group with a social enterprise model, takes a holistic approach to promoting financial literacy – an approach which rests on the foundation of empirical research using rigorous methodologies.

A good deal of the research upon which NFEC programs are based was conducted by the organization itself. The NFEC relies heavily on empirical data to guide curriculum development and measure campaign success. One example was a study that took place across 2012-13 wherein more than 1,300 students aged 15-18 responded to an online financial literacy test. These data were analyzed and compiled into a set of youth financial literacy statistics that are available on the NFEC website (www.FinancialEducatorsCouncil.org). According to these findings, young people’s need to build money management skill sets is growing – a total 72.7% of respondents scored lower than 70% on the test, with an average score of 58%.

The recent Great Recession in the U.S. served to underscore how poorly prepared our citizens have become to handle their personal finances. Although some recent indicators point to economic recovery, staggering problems such as bankruptcy, foreclosure, and crushing debt loads remain rampant. When the NFEC conducted a second research study with U.S. adults in 2012-13, the findings indicated that 96% of those who completed a web-based survey believed college students should be mandated to complete a financial education course before taking out a student loan. A further 93% of respondents expressed the opinion that the fact that students do not completely understand the terms and consequences of such loans was a “very big” or “big” problem. These are exactly the kinds of financial education statistics that form the impetus behind the NFEC’s state-of-the-art programming to teach money skills and accurately measure the impact of such programs.

The NFEC is working to address financial illiteracy in the U.S. and abroad by developing a comprehensive set of personal finance coursework for all ages. In addition, the organization offers tools to quantify the results of financial education and raise awareness about the financial literacy movement.