Resources on Personal Finance for Teens

If you have a desire to learn more about teaching personal finance for teens, you’ve landed in the right spot. Here you can gain access to some resources that explain the topics best suited for financial literacy programs for youth that really hit home, and the factors that have impact on teens’ finances.

How to Make Personal Finance for Teenagers Engaging

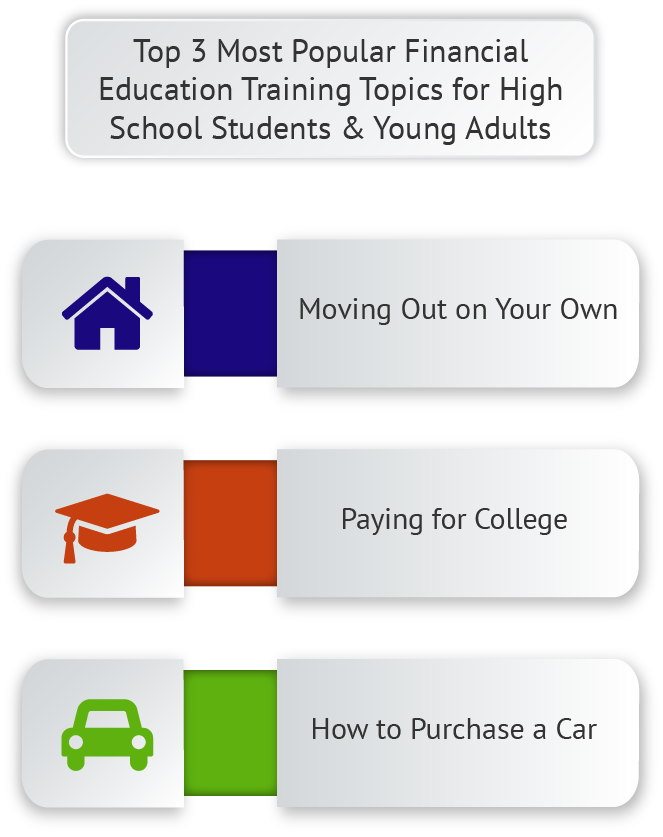

When teaching personal finance for teenagers, it’s important to focus the training around topics of particular interest to young people. Youth are likely to be facing certain life decisions that involve money. For example, teens are in the process of becoming independent, self-sufficient individuals. They will soon need to figure out and handle the expenses of living on their own. Workshops that cover goal-setting, budgeting, clarifying living expenses, insurance, credit, etc. are quite popular among the offerings of personal finance for teens.

Another topic of importance to teenagers is how to pay for higher education. Whether they plan to attend college, trade school, or on-the-job training, they’ll need to fund that education somehow. A personal finance course for college-bound students that focuses on college planning and budgeting, return on investment of higher education, career choices, and available funding streams will prove valuable for teens on this path.

Car-buying is a third option in personal finance for teens that captures their interest. Ninth and tenth graders will benefit from money management for teens training that includes how to set financial goals, budgeting before buying, the hidden expenses in car purchases, the loan application process, etc.

When presenting personal finance for teenagers, centering the subject matter around topics of particular interest to youth audiences is the best way to attract participation and keep them engaged and involved in the training.

Next Step: Get to Know the Audience

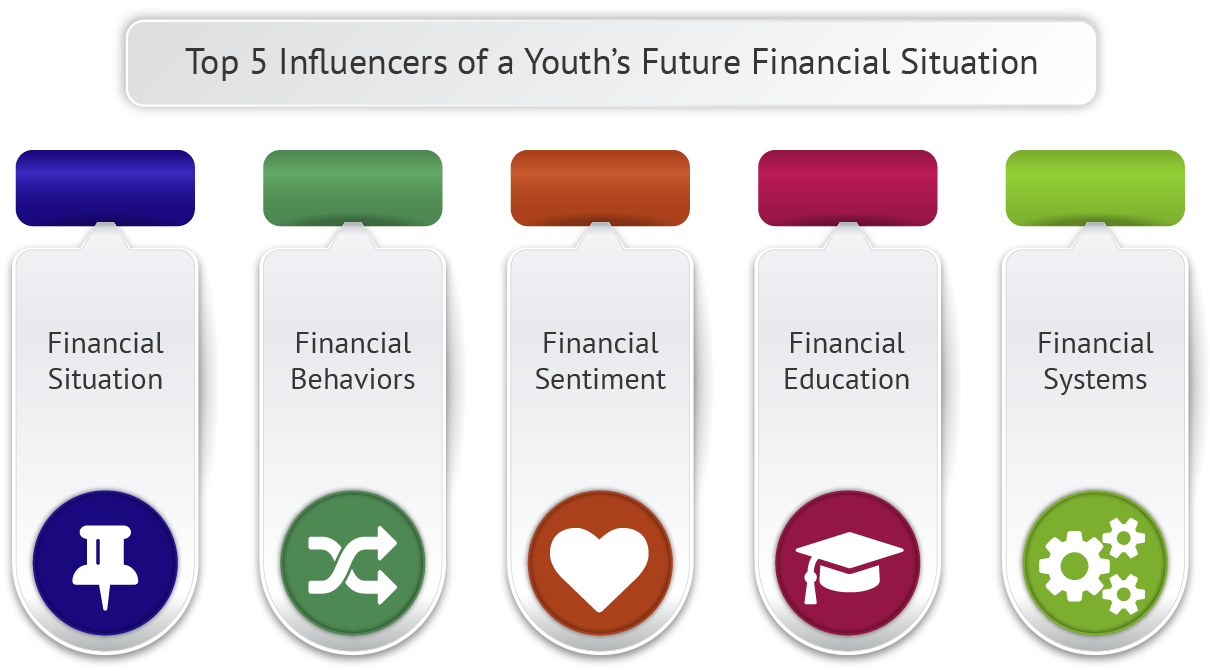

Teaching financial literacy to youth with maximum effect also requires understanding the challenges they face. The data show that children born into lower SES families probably will face greater barriers to achieving financial security than those born into families of higher SES. However, that doesn’t mean teens in low SES families have no hope. It might require extra effort, but they still have the chance to become financially healthy.

Another important factor to take into consideration is the strong effects of advertising on teenagers’ development. The negative effects of ads can be psychological or physiological in nature. Psychologically, marketing exposure encourages young people to adopt spending behaviors that may cause them financial problems down the line. Physiologically, youth are encouraged by advertising to engage in behaviors such as consuming sugary beverages and unhealthy fast food, or using tobacco products.

The various influences on young people – not just advertising but also parents, peers, and their environmental setting – coalesce into a particular set of attitudes, beliefs, and emotions around money. These financial sentiments should be addressed when teaching personal finance for teenagers.

Financial education for teenage audiences is gravely needed to help them navigate the complex financial world, like the myriad emerging online banks. However, public schools rarely offer training in personal finance for teens. By reading this article, you’ve demonstrated that you have an interest in helping fill this need.

Parents have one primary job: to help their children become independent, thriving adults. Regardless of demographics or education level, every parent can help his or her kids build important life skills for success. Placing emphasis on teaching personal finance for teenagers is a great place to start. Parents need to seize important opportunities—while their teenage children still live at home—to promote money skills they’ll need when they move out on their own. (And chances are you do want them to move out on their own.)

According to Pew Research Center, in 2012 21.6 million young adults aged 18 to 31 lived in the home of a parent (http://www.pewsocialtrends.org/files/2013/07/SDT-millennials-living-with-parents-07-2013.pdf). This group has become known as the “boomerang generation,” as many of the young adults are college graduates who bounce back home when they’re unsuccessful at landing a job. But what can a parent do to avoid having an unwanted roommate? An ounce of prevention is worth a pound of cure, and giving a sound foundation of money management for teens can make all the difference.

Even parents who never learned about money when they were young can help their kids pick up key personal finance skills. One excellent resource can be found by contacting the National Financial Educators Council (NFEC), a social enterprise organization that provides products and services designed to raise people’s financial competencies. For example, they have a personal finance curriculum to reach people from any background or age level.

When they’re still in high school, personal finance may be far from kids’ minds as they prepare for college or trade school. But unfortunately many young people will be unprepared to face the stark financial realities of living in the real world. More students drop out of college due to financial issues than ones who do so for academic reasons. That’s why parents should make sure to promote financial education for teenagers; otherwise, their kids may come back in debt, without a degree, and looking for a place to live.