Personal Finance Facts

Access to facts about personal finance, which include a wide range of statistics and financial tips, is necessary for personal financial success. Although it is beneficial for people to learn personal finance facts from friends, family, and a wide variety of trusted internet sources, the best place for interested parties to discover personal finance facts is an established financial literacy program, which can gather and distribute reliable information. While there is a lot of content that must be included in financial literacy education curriculums for participants to find success, the inclusion of personal finance facts in a necessity.

The Function of Personal Finance Facts

Facts about personal finance can range from data on the state of financial illiteracy in the nation to factual statements that can help customers save money on anything from their credit cards to their mortgages. While personal finance facts can be learned from a variety of sources—friends, family, neighbors, community events, social media, community institutions—personal finance course offered by a financial literacy initiative can provide the necessary structure to ensure that no crucial facts about personal finance are left unexplained.

Factors that Mold Personal Finance Behavior

Researchers at NBER demonstrated the positive relation between the average stock market participation between the individual’s community and the individual’s participation rate in the markets. This effect was proven to be stronger in more sociable communities. http://www.nber.org/papers/w13168.pdf

A statistically significant association was determined between negative financial habits, such as gambling among Australian youth, and the influence of peers and parents. https://www.sciencedirect.com/science/article/pii/S0140197103000137?via%3Dihub

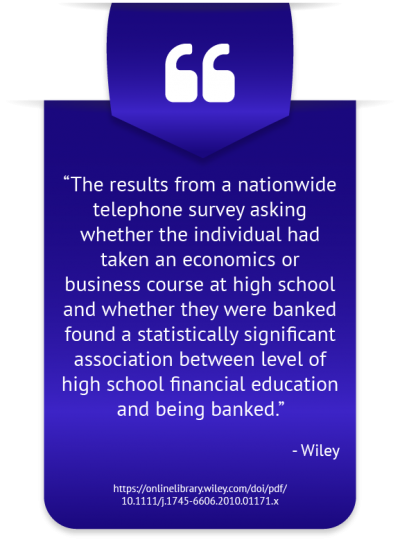

A team of researchers surveyed students at 15 geographically diverse colleges to assess financial knowledge and behavior. Student responses were organized into 1 of 6 categories based on the type of financial education policy a student’s home state had for high school. The categories ranged from a state with no standards at all to states that required a financial literacy course and assessment in high school. Students whose home states required financial education courses were found to be more likely to save, less likely to make late credit card payments, and more likely to take on a healthy amount of financial risk. While 1.3% of those with no state standards ‘maxed out’ their credit cards, only 0.7% of those with a required course and corresponding assessment ‘maxed out’ their credit cards. When asked if used a budget, 46.7% of those with no state standards replied yes while 52.9% of those with a course and assessment replied yes. https://www.nefe.org/Portals/0/WhatWeProvide/PrimaryResearch/PDF/Gutter_FinMgtPracticesofCollegeStudents_Final.pdf

Problems Caused By A Lack Of Financial Literacy

In a survey conducted by the National Financial Educators Council, 5.2% reported they had been turned down from a job due to a lack of financial knowledge, and 18.2% responded they were not sure. https://www.financialeducatorscouncil.org/financial-literacy-statistics

A 0.2 increase in standard deviation on a financial literacy score would result in a predicted additional $13,800 in new wealth. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3554245/pdf/nihms-400812.pdf

7.7% of those scoring in the lowest quartile of a basic financial literacy test participated in the stock market, while participation among those in the top quartile was 32.8%. http://www.nber.org/papers/w13565.pdf

18% of adults cited retiring without having enough money set aside as their top personal finance worry. https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

The average debt of students when they graduated from college rose from $18,550 (in 2004) to $28,950 (in 2014), an increase of 56 percent. https://ticas.org/sites/default/filesub_files/student_debt_and_the_class_of_2014_nr_0.pdf

The Benefits of Personal Finance Knowledge

Researchers asked individuals two sets of questions, one pertaining to basic financial literacy while the other related to advanced financial knowledge. The researchers then applied statistical techniques to construct indexes of financial knowledge. The probability of participating in the stock market increased 14 percentage points with a one standard deviation increase in advanced financial knowledge. In addition, a one standard deviation increase in basic financial literacy increases the probability of saving for retirement by 20 percentage points. https://www.dnb.nl/en/binaries/working%20paper%20313_tcm47-257145.pdf

The Canadian Task Force for Financial Literacy states effective programs will also use lessons gleaned from behavioral economics to recognize the disconnect between knowledge gained during lessons and real world application of that knowledge to improve program participants’ financial well being. http://publications.gc.ca/collections/collection_2011/fin/F2-198-2011-eng.pdf

The Jump$tart coalition recommends that materials correlate to standards but forth by states or leading councils and associations. Resources provided to students should be written in plain language when possible, clearly defining any obscure words. https://www.jumpstart.org

The Need for Facts About Personal Finance

Personal finance facts are an excellent pool of knowledge that individuals can draw from in order to make healthy financial decisions. These personal finance quotes are often employed to save money on monthly expenses and on one-time expenses such as car purchases. While blogs and community networks are an invaluable source of learning about personal finance topics, carefully constructed financial literacy curriculums have the benefit of covering all the necessary topics within personal finance standards in a manner that facilitates true understanding.

[1] National Financial Educators Council, Personal Finance Case Studies