Given today’s uncertain economic climate, gaining a fundamental money management education has become vital. A good personal finance course will be one that not only covers basic money lessons, but that offers practical tips for applying the information to one’s day-to-day life. Mastering efficient methods for managing money may be the single most important life skill a person can learn.

It’s critically important that finance training courses set forth information in a way that people can actually use. For example, money management topics can be taught in much the same way as driver’s education. When you learn to drive a car, you might study written materials first to learn the rules of the road, but most of the learning process is done through practice. Practicing ways handle your finances is just as valuable.

As you learn basic money management skills, good financial literacy courses will train you to apply them to real-world situations. In the case of money managing, the coursework might guide you to create a budget. Simply put, a budget is a plan for handling your money. To return to the driving example, it’s like drawing a roadmap for your personal finances.

Your personal finance class might illustrate the need to budget by mentioning these advantages:

- Control. Having a budget puts you in the financial “driver’s seat.”

- Organization. Having your finances in order keeps you aware of every penny.

- More money. Sticking within a budget leaves you with extra at the end of the month.

- Opportunities. Having more money means you can take advantage of opportunity as it arises.

A big part of budgeting is adopting good spending and savings habits. While these skills are just one piece of personal finance wellness, they are extremely important. Any worthwhile personal finance books or courses will include a budgeting lesson early on.

Personal Finance Course

The Money XLive online personal finance course and multimedia learning center engages today’s youth in the learning process. This is not the typical ‘boring’ online program that just offers a series of articles. The MXL coursework features exclusive celebrity videos, interactive tools, comprehensive guides, testing and motivates participants to take action. This program is aligned with national financial education standards while remaining practical in nature so our youth can utilize these lessons in the ‘real world’.

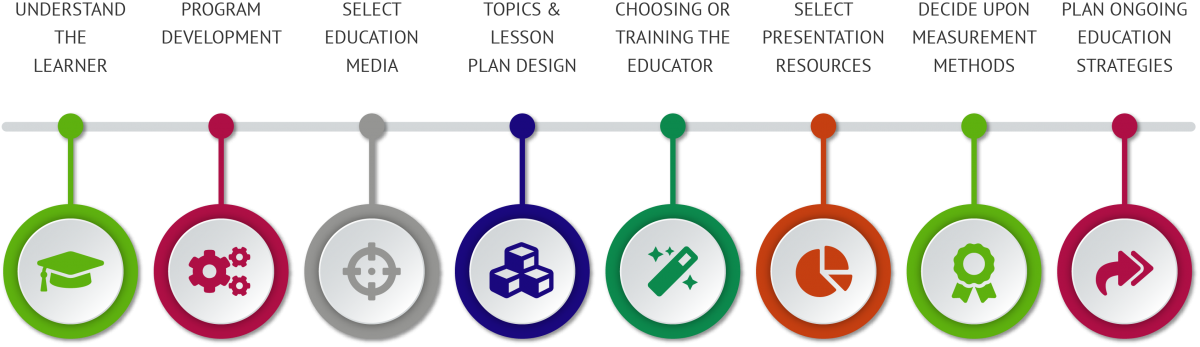

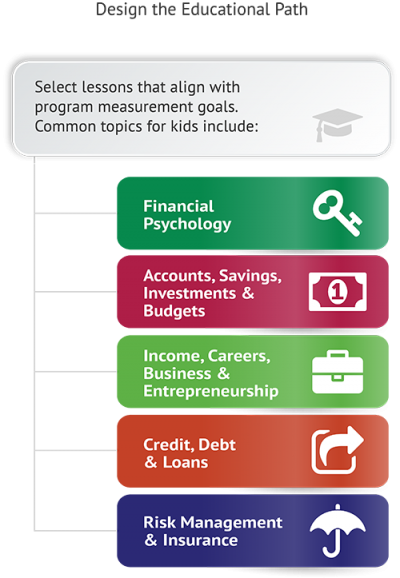

This personal finance course covers 10 area, including: financial psychology, accounts & budgeting, skill growth, risk management, credit, savings & investing, social entrepreneurship, income, business relations and money management.

By the time students graduate the Money XLive coursework, they have completed a series of activities that help them build a solid financial foundation. Participants have a budget in place, a long-term financial plan, financial goals, credit plan, understand what skills will help them and they possess more financial knowledge than the average person of any age.

This video and activity-based financial literacy workshop will keep your students entertained and wanting to learn more.

- Over 25 educational and entertaining videos.

- 15 exclusive celebrity video interviews.

- Quick tip section for fast, convenient learning.

- Quizzes and surveys to measure literacy growth.

- Online testing and surveys.

- 100% independent, non-bias, training tools.

- A sixteen step companion course.

By now you know, the Money XLive Personal Finance Course will help secure your children’s future. More information on the MXL personal finance online course can be viewed here. Give your children or the youth you serve the advantage many of us wish we’d had—a practical financial education course. The NFEC commends your interest in the MXL virtual learning center that is helping to secure the future of today’s youth.

Personal Finance Courses for Teens and College Students

Why are 60+% of college graduates are planning on moving back home with their parents? It boils down to the fact they have not received a practical financial education at any time in their school career. Today, with uncertain economic times and high unemployment rates, it is more important than ever young adults are prepared for the financial real world that awaits them when they graduate.

For the younger generation today, they need achieve financial security because the entitlement programs that serve our retirees will be drastically cut. There is a strong possibility that the social security program won’t be around so the need for them to achieve financial independence is critical. A study by the GAO (Government Accountability Office) predicts that 33% of workers will have zero saved in a 401k style account by 2050. The National Association of State Boards of Education states ‘most workers aren’t participating sufficiently enough to allow comfortable retirement’.

With the lifespan of this generation longer than ever before our kids need to start preparing early. The baby boomer generation is nearing retirement age and most analysts predict that Social Security will be nothing but a memory by the time your teen- and college-aged children are ready to retire.

Providing personal finance courses is a proactive solution. Just like early health screening, financial education courses can prevent the consequences that accompany financial illiteracy. Even today’s youth are aware that they need to start saving for their future; yet the average student has no idea where to start. Providing money management training to kids early in life can help them achieve a state of financial wellness.

Parents realize the importance of a financial education but most don’t realize that this is not taught in school. It is important for parents understand how important knowing basic personal finance lessons is for their children’s future and enroll them in a professional level financial literacy courses before they move out on their own.

Personal savings are at an all time low and credit card debt is hitting new highs. The average American spends MORE than they earn. Rising housing costs, combined with increasing bankruptcies and foreclosures, are sending families into financial crisis. This is the reality your child faces once they’re on their own, all because their parents and grandparents before them were not taught personal money management skills.

So the solution is simply. Ensure your children and the youth you serve receive a personal finance course. It is an investment that will provide them substantial returns in their future relationships, overall wellness, health, happiness and financial security.

Savings is Key Focus of Personal Finance Courses

In today’s world, people of all ages—from pre-kindergarten through mature adulthood—would benefit from learning more about money. Fortunately personal finance courses have become increasingly more available to provide such vital education. One primary focus of such a program should be teaching people the basics of a savings plan. Positive savings habits set the stage for a secure financial future.

According to the National Financial Educators Council, a personal finance course should cover savings very early in the coursework. A healthy approach to saving money underpins a financially secure lifestyle. When people set money aside each month, even a small amount, they construct a foundation for building future wealth, while keeping opportunities to enjoy life now.

In the NFEC’s finance training course they suggest that savings should be separated into three categories: 1) an emergency fund equal to six months’ worth of essential expenses; 2) a short-term savings account to pay for fun activities; and 3) long-term savings where you hold money for future investments.

How much should you save? The recommendation set forward in the NFEC program and personal finance books is a 15-15 split: 15% of your income for fun, and 15% for long-term investments. This plan should go into place after you have saved enough in your emergency fund to last six months. If you find 30% a difficult target, try either cutting down on expenses or find ways to earn more income.

A savings plan is the backbone of one’s financial future. Thanks to compounding interest, a person who starts saving early can see even a small monthly amount grow into a fortune by the time he or she reaches middle age. That’s why the NFEC places key emphasis on savings in programs to teach personal finance for kids of all ages.