Techniques to Maximize Financial Literacy for Young Adults

Coordinating programs to increase financial literacy for young adults requires specific knowledge regarding best topics to present and the distinctive personal finance situations young people are likely to come across. If you’re interested to embark on financial literacy programs for youth and young adults, you will find invaluable information on this page.

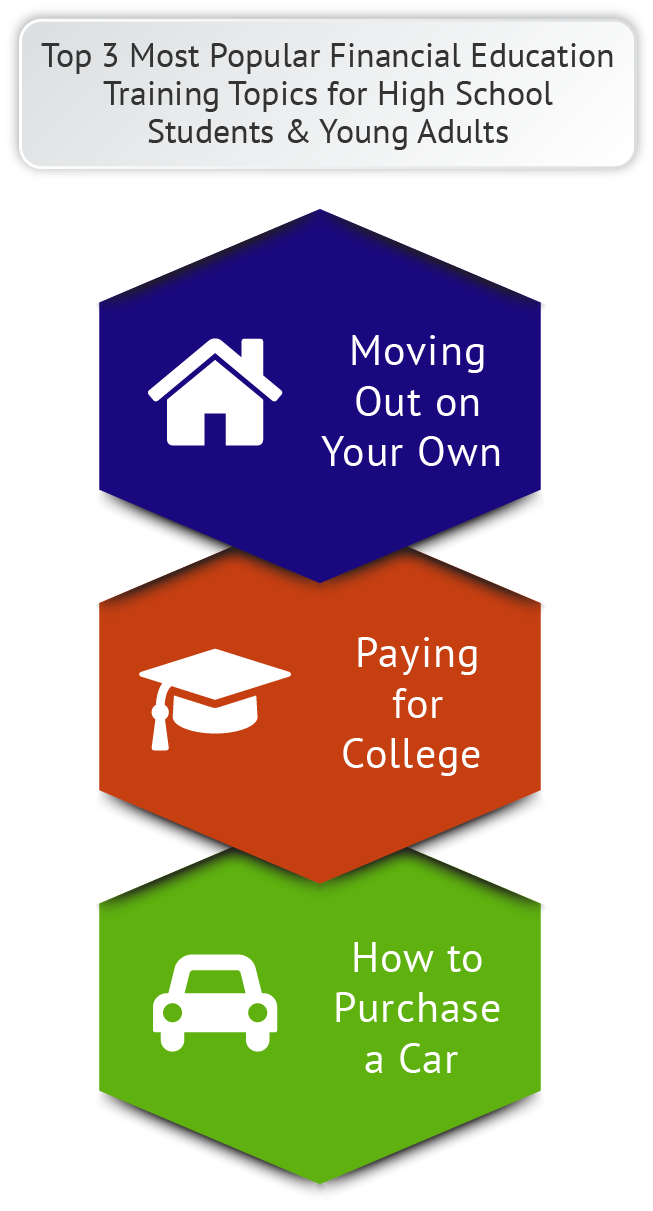

First Step: Optimal Topics for Young Adult Financial Education

Raising financial literacy for young adults demands that you offer them information that will have true relevance to the real-world decisions they must undertake. We recommend presenting subject matter that will prepare them to move out into their own living situations, buy a car and, for college-bound youth, pay for higher schooling.

Assist young people to get ready for the requirements of adult life by teaching subjects such as finding a property to rent or buy, showing landlords that they are responsible, developing smart goals and budgets, classifying and preparing to meet all their expenses – e.g. rent, insurance, car payments, utility bills, sustenance, and entertainment. All these topics are important money management lessons for young adults.

Aid young adults through the car-purchasing process by presenting guidelines for finding a vehicle that fits within their goals and budgets. Then build their capabilities to dicker with car salespeople for the best price and terms, buy adequate auto insurance, apply and qualify for a car loan, and sort out all the less obvious costs of vehicle ownership.

A personal finance class for high school kids or older should guide teens toward a viable higher education option by introducing them to college planning, the ROI of a given college major and career path, and how to budget for one’s schooling pursuits. Show them the options to fund school that don’t need to be paid back, such as scholarships or government grants, before they ever sign onto a student loan.

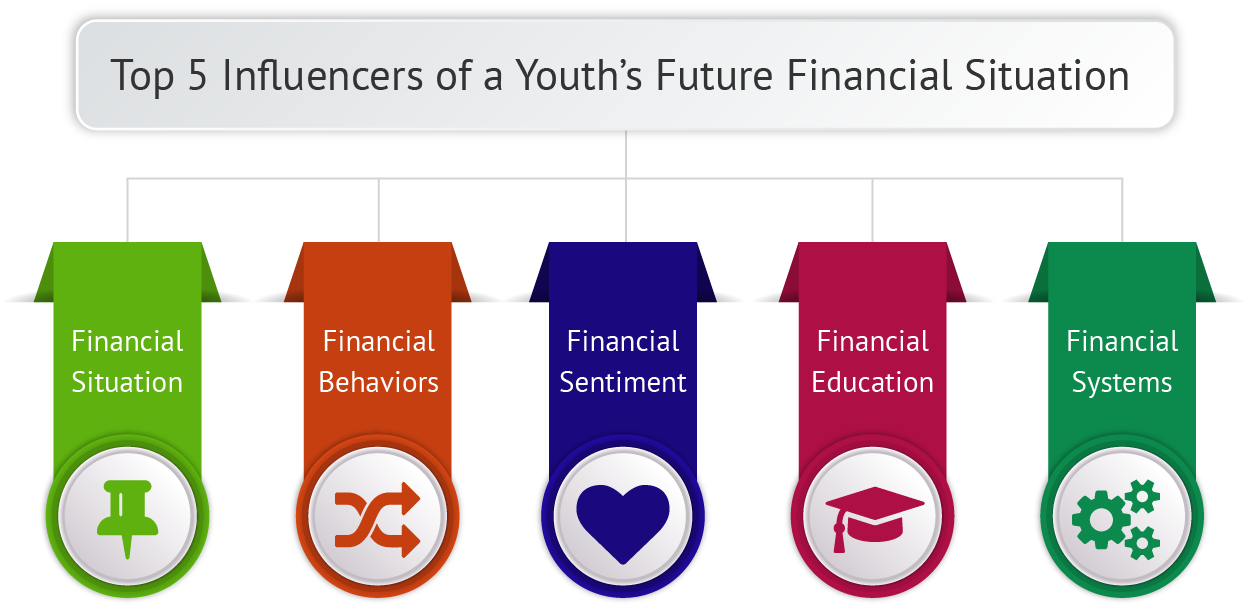

Good Financial Education for Young Adults Must Concentrate on their Challenges

To teach financial education for young adults, you should emphasize how they can meet the singular challenges young people encounter in today’s world. There are five major influences on how a young adult’s personal finance situation is likely to evolve into the future.

First, has the young adult set up financial systems to organize their money and classify their budget line items? Everyone needs – at minimum – savings, checking, and retirement accounts to manage money effectively. For young adults who fit into the “Gen Z” age group, take a look at these apps to make this process more interesting.

Second, explore the level of financial education for young adults that’s been available to a given audience. Research indicates that most teens have not been taught the essentials of personal finance management either at home or in school. And even those few who are exposed to money instruction probably did not receive the highest quality of training.

Third, what emotions, attitudes, and beliefs about finances have been shaped among these young adults? This relationship with money is called “financial sentiment,” and serves as an important indicator of how these students will manage their funds as they mature.

The fourth challenge is posed by young adults’ exposure to advertising and other manipulators. Pressures from friends, the social environment, parents’ financial capabilities, and marketing messages all exert powerful influence to mold young people’s financial behaviors.

The fifth and last issue to emphasize is where these young adults came from. Whether their parents experienced high or low socioeconomic status, and how financially secure the child rearing environment was, can deeply affect their future financial situations.

Placing focus on dealing with these central issues and life events is the best way to build a strong financial literacy curriculum for young adults.

Financial Literacy for Young Adults Today Avoids Big Problems Tomorrow

Financial Education Young Adults

If parents and educators fail to teach kids about money today, they may face much bigger problems down the road. Without financial education for young adults, those youth may emerge from college buried in student and credit card debt, and face a zero balance savings account by age 40.

Providing a strong foundation in money management for young adults today will help parents avoid having their kids move back home after college graduation—a disturbing trend that now happens nearly 60% of the time. Teaching teens about money before they go off to university will play an instrumental role in giving them a brighter, more independent future.

The main purpose in teaching financial education for kids is to prepare them before they head off to college. Before they step onto campus, young people should be financially prepared for the challenges they will face. That way they can meet any money struggles head-on with a good plan in place for handling them, and avoid money problems that can escalate out of control.

Teens need to learn about money in a practical way that gets them interested to learn. That’s why one of the first goals in financial education is to relate money to lifestyle. If young people can relate a lesson to their individual lives, they’re more likely to internalize the information and apply the skills to real-world situations.

A good example of a practical money lesson is showing youth the magic of compounding interest. When they realize that investing only $100 a month starting when they’re young could add up to more than a million dollars later on, you’re likely to capture their attention. This lesson and a variety of other practical financial education resources will give kids a strong advantage over their peers who do not learn basic money skills.

Parents and teachers should become financial educators along with the other important life skills they teach. This undertaking will help them avoid much bigger problems when teens become young adults.

Spreading Financial Literacy for Young Adults Makes Huge Impact

One of the most profound ways in which we can make a positive difference in someone’s life is by spreading the message of financial literacy for young adults. Today’s emerging generation faces a shaky financial future where pension funds and Social Security may be a thing of the past. That means it’s more important than ever before to teach kids about money.

Few schools or parents undertake to teach kids money management skills. That is a classic irony: the subject that will benefit young people the most is the one least likely to be taught. Yet providing money management tips for young adults is quicker and easier than learning high school algebra. It’s just a matter of picking up some basic skills and effective teaching methods.

Following are a few tips to get you started teaching financial literacy for kids:

Relate money to dreams and goals. If kids are really going to learn about finances, they need to internalize the lessons to the point where they form positive money habits. Toward that end, it’s important not to focus on the money itself, but on what money gets you. Help youth identify their dreams and desired lifestyles. Then show them how money lessons relate to achieving those goals.

Help teens recognize opportunity. When the economy takes a downturn, people who are financially aware make investments toward increasing their net worth in the long-term. A simple lesson in market cycles and recognizing how to take advantage of investment trends will go a long way toward securing a young adult’s financial future.

Create a savings plan. Financial literacy for college students requires having a workable budget and a savings mindset. Youth must form good savings and spending habits in order to get by on limited funds while in college or university.

These tips for sharing money management skills with teens and young adults have the potential to make a huge impact on those young people’s lives, thus strengthening our future generations.