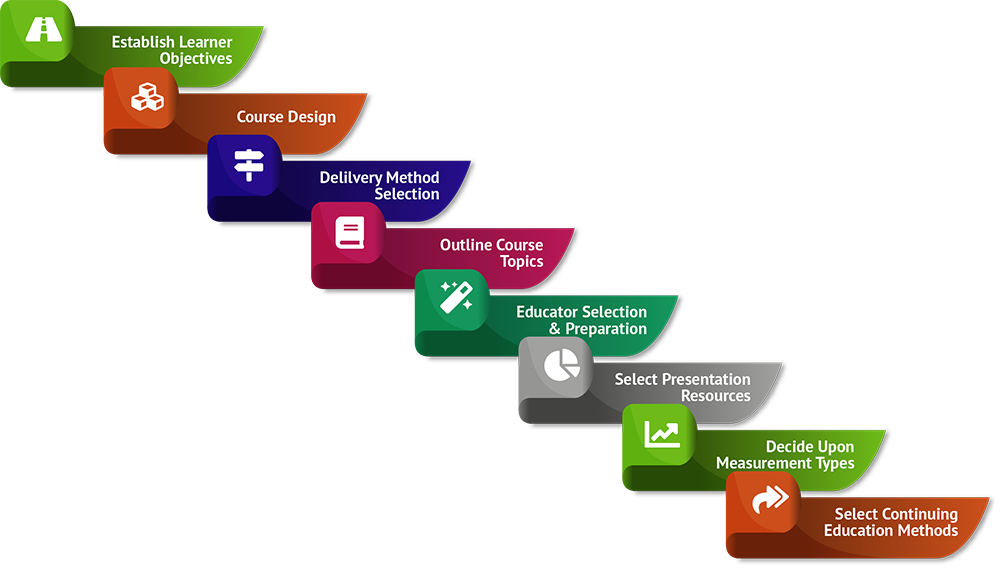

The Optimal Eight Ways of Teaching Children Money Management

It’s a topic on many people’s minds these days: Teaching Children Money Management in a way that helps secure their futures. The pages you’ll find here offer an eight-step plan for Teaching Children Money Management Lessons efficiently and according to the best practices indicated by research evidence.

Teaching Children Money Management Lessons for Maximum Impact

1. Methods and Resources for Teaching Children Money Management

The resources found here will guide you through Teaching Children Money Management, according to the effective process described in the example below:

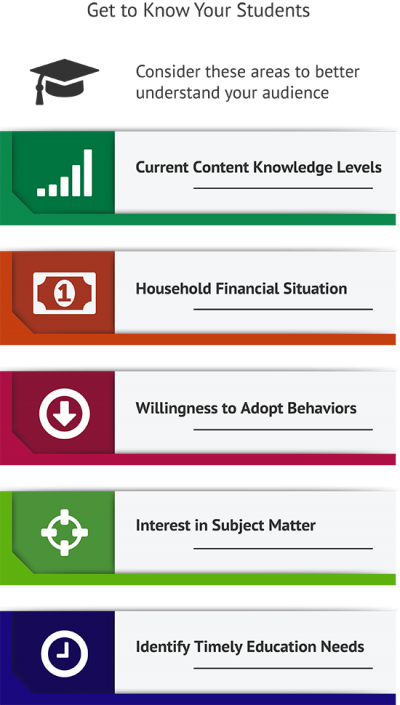

Charles Wright, who led a youth group at St. Mark’s Methodist Church, was interested in Teaching Children Money Management so he could educate the youth at St. Mark’s about personal finance. The 24 kids in Charles’s church group were mainly from middle-class families in their Northern California community, and ranged in age from 12 – 16. Although Charles had an interest in Teaching Children Money Management Lessons, he was unaware how much financial education the kids were getting at home or at school. He decided to give them a brief financial literacy test to determine their knowledge levels. Results of the test showed that the children really needed to learn about why savings was important and basic economic systems.

2. Clarifying First Goals for Teaching Children Money Management

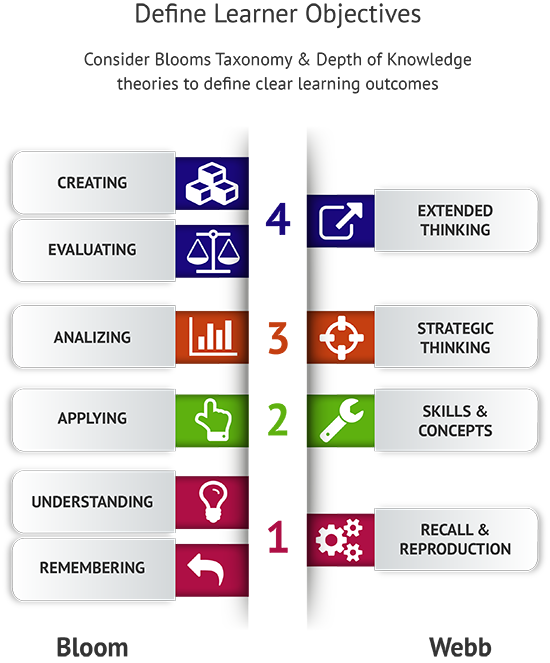

Now that Charles knew his youth group needed to learn how to save, he set an initial goal of doing an educational program with them to clarify savings benefits and go over the basics of how economic systems work. The group met for an hour every Wednesday evening, so Charles opted to set aside one of those meetings for the training. If the kids liked it, he could continue spending one Wednesday a month Teaching Children Money Management. For the first hour, Charles thought the youth could get to “Understand” on Bloom’s Taxonomy – that is, being able to demonstrate comprehension of the core concepts.

3. Instructional Pace and Delivery: What are the Options?

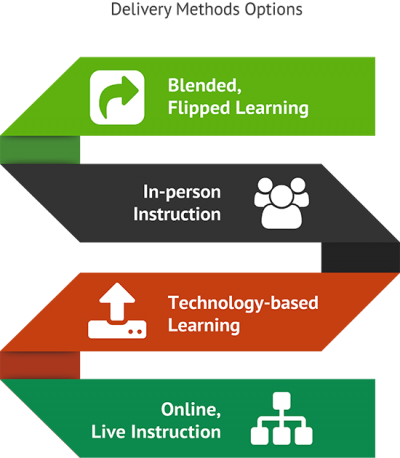

Charles now understood his first objective and continuing goals. The next phase involved choosing how to go about Teaching Children Money Management Lessons. Charles chose timeline-based pacing to fit the lessons into his one-hour time slot. Because they just had a little time, he decided to adopt a flipped instruction model: have the kids watch a video at home on their own time, and then do an activity together during their meeting.

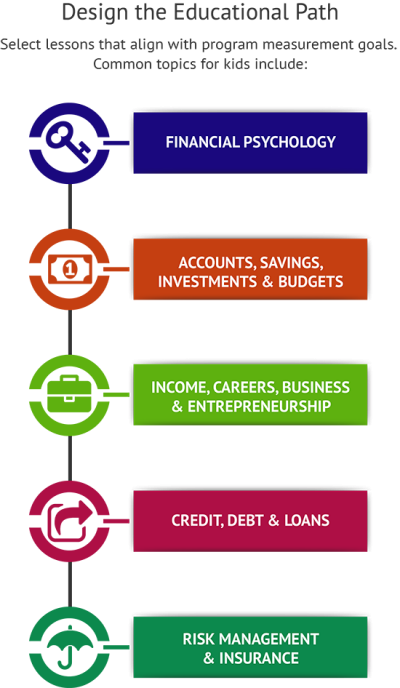

4. Primary Needs for Teaching Children Money Management Lessons Drive the Lesson Choices

Charles already knew his audience’s primary need: to learn the importance of saving and fundamental economic principles. That’s why he chose to focus his first stab at Teaching Children Money Management on savings and economic/government influences on money. Charles believed his goal of getting the kids to the “Understand” tier on Bloom’s Taxonomy could be reached by choosing topics relevant to the children’s lives and situations.

5. Educators Must be Qualified, Engaging, Available

At the fifth step Charles needed to select a highly-qualified educator to present the materials – a person with both personal finance knowledge and superb teaching skills. His idea was to hire the educator to record the video, and then Charles would lead the activity at the youth group meeting. As luck would have it, his pastor told him that an NFEC-Certified Financial Education Instructor was a St. Mark’s member. Charles approached her, and found that she was more than willing to record a video for Teaching Children Money.

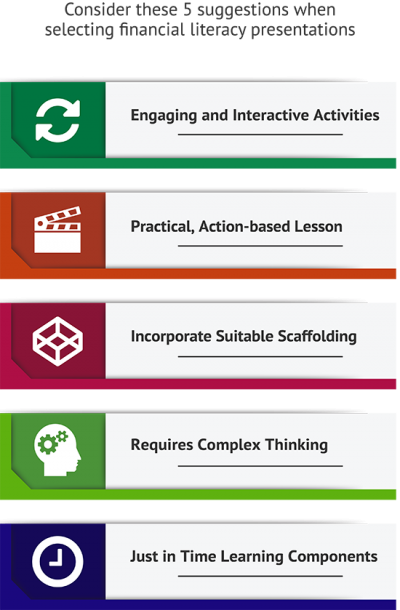

6. Qualities to Look for in a Curriculum for Teaching Children Money Management Lessons

The curriculum qualities Charles wanted were activity-based lessons for Teaching Children Money Management, with engaging and interactive activities. He achieved everything he needed by locating a widely-recognized curriculum program that incorporated practical, action-based lessons and just-in-time learning segments to address specific topics of interest.

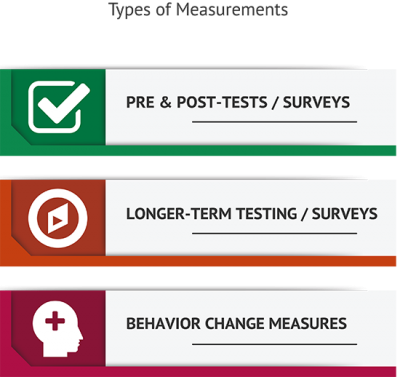

7. What do the Results Indicate? Measurement is Essential

As we mentioned, Charles had 24 children in his youth group. Out of the 24, all of them (100%) reported watching the video at home. A total of 22 (91.7%) were present at the meeting and participated in the activity designed for Teaching Children Money Management Lessons. After they did the fun activity, Charles re-administered the same test he’d used in the beginning. The kids’ scores improved a lot – on average, by about 28%. Charles reported the impact at next Sunday’s service, to let the congregation know how well the lessons were working.

8. Follow the Initial Experience with Longer-term Encouragement

After the initial experience was over, Charles was still excited about Teaching Children Money Management. He knew one meeting would be far from enough. He handed out participation awards after the first activity. Then he arranged for follow-up sessions to be held once a month at the Wednesday evening youth group meetings. Over time, this continuing education would help set the kids up for a bright future.