Student Loan Debt Petition: Stop the Exploitation of Minors

Many youths today feel that college graduation is the first step toward achieving a better life and working toward their personal dreams. But too many of our nation’s college graduates face a student loan debt load that will crush those dreams.

The current Federal Student Loan program asks young college hopefuls to make decisions that will significantly impact their finances before they even know how to balance a checkbook or calculate interest.

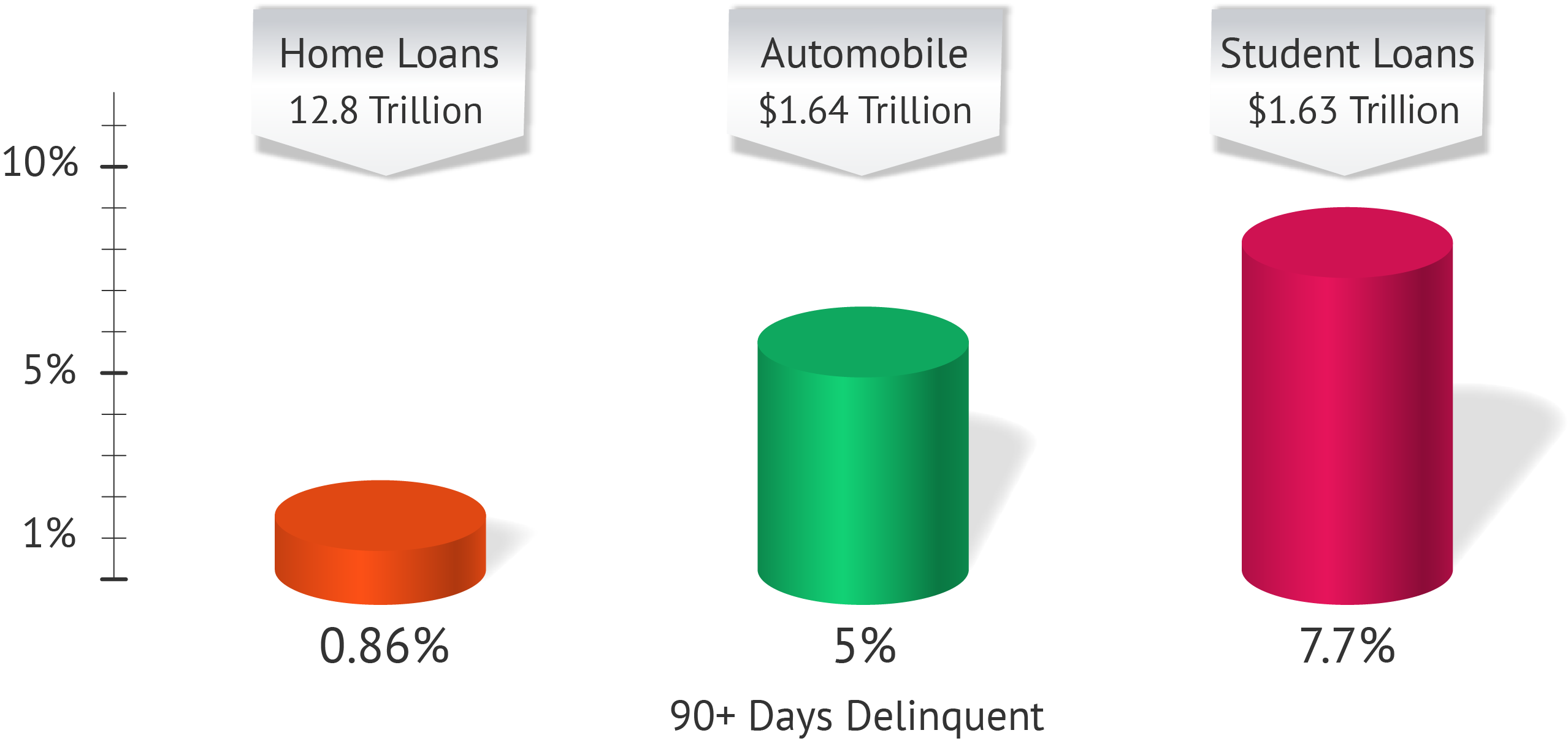

This campaign is focused on the practice of providing federally-backed student loans to 17-year-old students. Student loans have the highest default rates compared to other consumer loans (credit card, auto, home); yet all those debts require the person be 18 years old.

Petition: Stop Exploiting Minors in Student Loan Traps

I want to help 17-year-old minors avoid the problems that result from student loan debt.

I support requiring college-bound students who are 17 years old to prove that they understand key financial concepts before they commit to federally-backed student loan debt.

Data from: Student Loan Crisis

Asking Minors to Commit to Long-term Loans

What does a 17-year-old know about loans, paying bills, and accumulating interest? Not much, according to most data.

Today’s youth lack basic financial skills. Most teens fail even a basic personal finance test and graduate from high school without any financial education training. The majority of adults lack the capabilities to understand the impact of loans on their overall finances, repayment period, and total loan cost.

Most students entering college cannot legally rent a car or drink alcohol. Is it ethical to ask them to sign loan documents committing to years or even decades of debt?

Goal of Petition: Stop Student Loan Exploitation of Minors

The goal of this petition is to show support for a program that requires 17-year-old kids to complete financial education coursework before they commit to a Federal Student Loan.

What we advocate is that students be required to have the basic knowledge to understand what they’re signing. They should demonstrate that they possess the knowledge they need to make financial decisions that are best for their long-term futures. This knowledge base would include an understanding of repayment terms, return on investment of loan decisions, and risk of debt, among other fundamental personal finance topics.

Why this Petition Focuses Only on Loans to 17-year-olds

The focus on minors opens up opportunities to enlist the critical mass needed to propel this campaign forward. By connecting with key policymakers, we hope to save future children from promising to pay the type of consumer loan that has the highest default rate.

To support our policymakers, the NFEC drafted legislation, the College Student Protection and Financial Education Act, to enlist politicians in the effort to proactively address this national crisis.

This legislation proposes a preventive model similar to the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, which requires people to get budget counseling before they can file bankruptcy and financial education after they file.

Legislative Change: 1992 Higher Education Act

“In 1992 the Higher Education Act was amended to permit eligible students, defined as per Title IV regulations, to sign promissory notes for their own Federal student loans. As such, student loans represent one of the few exceptions to the so-called ‘defense of infancy.’

“The specific citation is section 484A(b)(2) of the Higher Education Act of 1965 (20 USC 1091a(b)(2)), and applies to Stafford, PLUS, and Consolidation Loans. Several states have also passed similar laws that consider minors to be competent to enter into a contract for an education loan. This legislation extends similar protection to private and non-federal loans.”