Training in Financial Literacy for Elementary Students

Are you concerned about raising financial literacy for elementary students, but don’t know how to get started? The resources and tips on this website are designed to help you understand how kids are influenced and how best to reach them at various life stages – the top ways to promote financial literacy for kids.

Understand the Pressures that Affect Personal Financial Literacy for Elementary Students

Kids are subject to pressure from their peers, modeling from their parents, psychosocial factors, marketing pushes, and environmental influences from their area of residence. All these pressures affect how we teach financial literacy for elementary students.

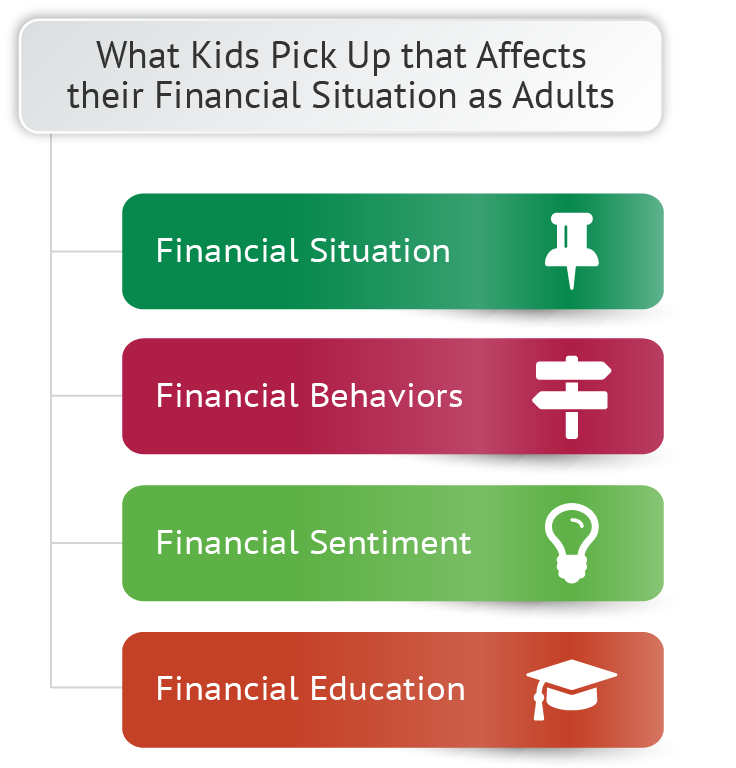

Initially, look at the financial situations into which kids are born. The childhood money environment has tremendous impact on a child’s future personal finances. If the parents are poor, or have difficulty managing their own money, children see that and can be influenced in the wrong direction. If the parents are well-off and/or savvy about personal finance, the children have a better chance of picking up positive habits.

Then consider how financial literacy for elementary students might help them develop positive behavior patterns. Kids learn easily by absorbing information. According to a study at Brown University, kids’ habits take root by age 9 and are likely to stick throughout life. https://www.huffpost.com

Marketing to kids uses a wide variety of channels and techniques, and there’s evidence that kids are heavily influenced by advertising. Stepping in early to help kids form positive habits for money handling is essential. Furthermore, at a young age, children are building their emotional and psychological relationships with money. This financial sentiment often carries on into adulthood and influences their capability to handle personal finances in the future.

It’s a shame that so few kids will undergo education that promotes personal financial literacy for elementary students. Even at the high school level, you’ll find that few states require teaching kids curriculum about money. This important need must be addressed.

Adjust Financial Literacy for Elementary Students to their Cognitive Level

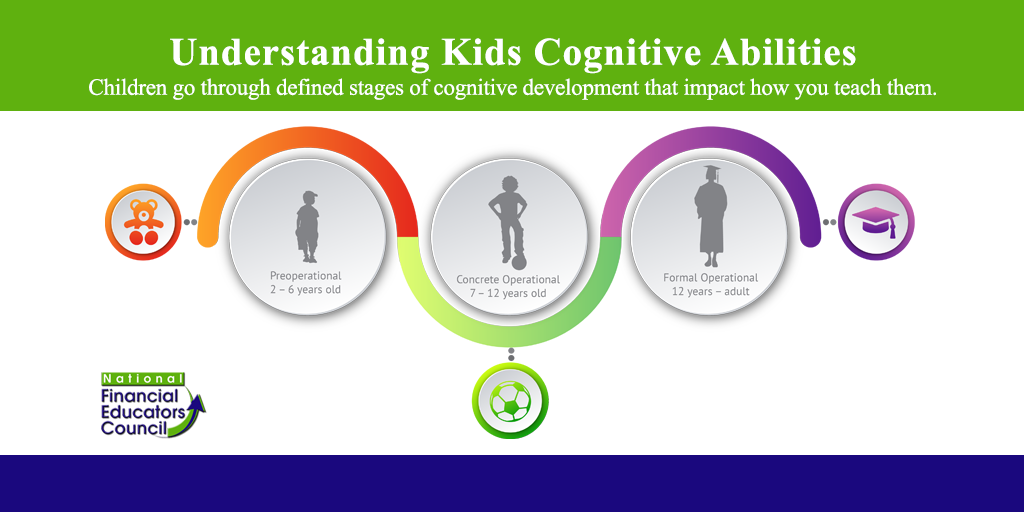

Effective instruction in personal financial literacy for elementary students should be adapted to fit the level of cognitive thinking of which they’re capable. As Piaget stipulates, kids who are 2 to 6 years old are preoperational. At this stage of development, many children enjoy playing “house.” You could build on that game to create financial literacy lessons they would enjoy.

Children aged 7 through 11 are “concrete operational” and can comprehend number relationships and values. Activities that present the basic ideas of production and consumption, measurement patterns, and low-level data analysis are in order. And kids age 12 and up, the “formal operational” stage, can think abstractly and benefit from complex project-based learning modes. You might present them with case studies that introduce a character facing financial problems, and have the students brainstorm ways to address those problems.

The upshot of all this is that effectively teaching personal finance in schools depends upon molding good behaviors before they have a chance to pick up negative ones. For some thoughts about the best personal finance books for children, check out this link from Investopedia.