Financial Literacy Class Design: A How-To Guide

Are you online in search of help organizing your very own financial literacy class? Congratulations! Your search is finally over. You’ve managed to come across our step-by-step walkthrough that details just how you can achieve this goal – and develop the best program for your particular needs.

Planning a Financial Literacy Class

A Pragmatic Path to Achieving

In the example that follows, you can see an example of a professional who got some much-needed help to pull off a series of successful financial education classes:

Archie is the head coordinator at a community center, where he oversees 12 employees – all of whom are under the age of 25. After multiple employees asked him some questions about basic personal finance matters, he opted to begin planning a financial literacy class description and accompanying course that would be beneficial to all of them. Everyone in this group was already quite familiar with him, as was the topic of money management. He was still missing some critical pieces, however.

After doing an informal survey with a handful of the team members, he immediately realized that most of them needed basic resources on just the core fundamentals of personal finance.

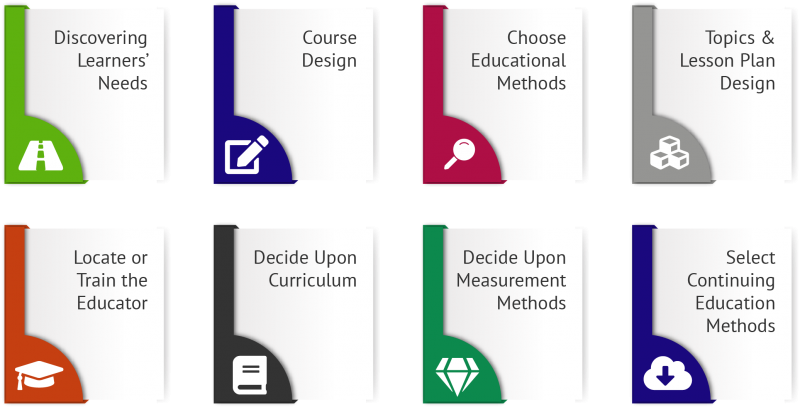

Financial Literacy Class Description: Defining Goals

With this specific financial literacy class, his end goal was for the group to reach the “Skills & Concepts” level of understanding with confidence.

Developing a Financial Literacy Class Description

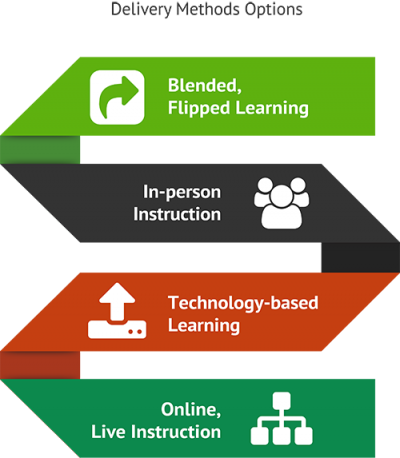

After Archie had defined his practical goals, the delivery method was what he needed to decide next. Given this group’s limited amount of availability, he knew that an online-based financial literacy class would be ideal.

Defining a Clear Focus for Your Financial Literacy Class

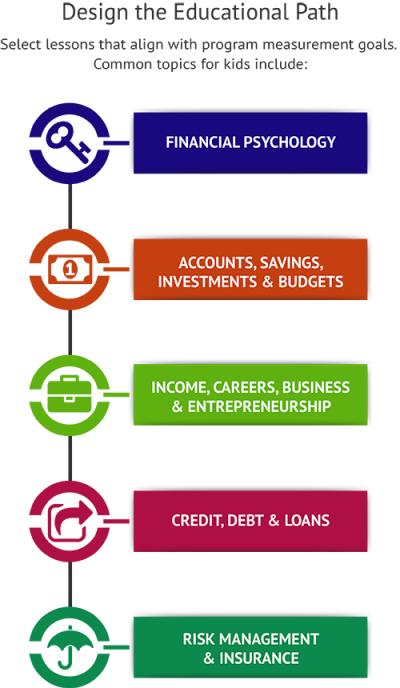

Archie, at that point in his journey, needed to figure out a more well-defined core focus of his financial literacy class description. Most of this group were young professionals, so he decided to focus the course on retirement planning and improving their credit scores.

Getting Expert Assistance

Archie, at that point in the process, needed to reach out to a qualified educator who could assist him in presenting his financial education classes. The instructor he was looking for would need to both skilled in teaching and knowledgeable on the topic.

The educator he ended up going with for the financial literacy class was a Certified Financial Education Instructor (CFEI) affiliated with NFEC.

Format: Financial Education Classes

Archie needed financial literacy class that would be successful, despite the group’s schedule limitations. With that in mind, he chose to build a flexible solution that’s broken up into easy-to-digest units that could be done on the employees’ own free time.

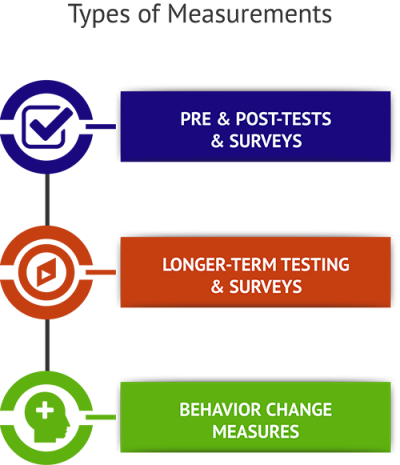

Diving into the Data

Of the 12 team members for whom he designed the financial literacy class description, 11 managed to successfully complete the whole course with an average knowledge growth rate of 12%. Archie’s next move was to compile the resulting data and generate an in-depth report that he could use to verifiably demonstrate the positive impact. He defined financial literacy achievements and highlighted the success in the report.

Progress & Success: Getting Recognition

Archie realized that this group of employees would be able to reach their highest potential if they were to receive ongoing support from him. When the first financial literacy class came to an end, he sent them all individual emails congratulating them on finishing the program – and encouraging them to continue their learning journey.

He ended up deciding to keep offering follow-up courses to everyone in the group, once monthly, so that they could more easily maintain the wealth of knowledge they gained through the first of his financial education classes.