Why We Need to Teach Financial Literacy in Schools

Financial literacy courses in schools are absolutely necessary. As awareness grows about why we need to teach financial literacy in schools, the idea is becoming more accepted, but we still have a long way to go. It is important to move ahead with this movement as quickly as possible, while maintaining high-quality standards and tracking the data. The answers to the question of why we need to teach financial literacy in schools are numerous and far-reaching. The deep underlying principle is that if even one person misses out on learning these fundamentally necessary skills for a successful life, the unfortunate consequences might be as severe as lifelong poverty for many generations to come.

Financial Literacy Must Be Taught in Schools

When there are an ample amount of financial education programs operating outside of school, how do we teach financial literacy in schools and how do financial educators respond to inquiries as to why we need to teach financial literacy in schools? The answer lies in the fact that not all students will have access to nor will all students attend enrichment programs outside of their prescribed school curriculum. Art and music classes, although not as important as financial literacy skills, are offered in many communities, but only a handful of parents enroll their children in such classes.

Teaching Financial Literacy in School has a Lifelong Impact

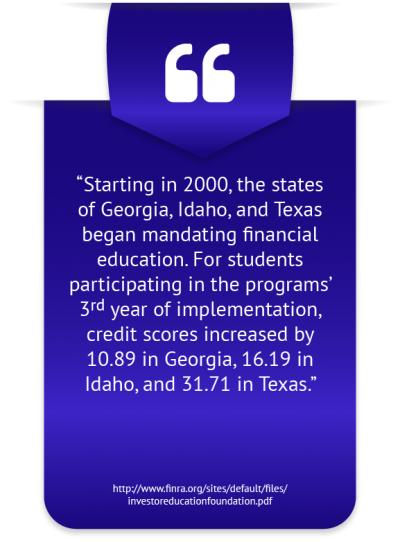

Researchers took advantage of a survey recording self-reported savings rates, as measured by amount of unspent take-home pay along with voluntary deferrals (e.g. 401(k) plan), and the state the respondent went to high school in. This is used to determine whether state mandated financial education curricula have an impact on the amount individuals save. Those entering high school five years after the implementation of the mandate had a savings rate of 1.5 percentage points higher than for students not exposed to a mandate (National Bureau of Economic Research). http://www.nber.org/papers/w6085.pdf

The results from a nationwide telephone survey asking whether the individual had taken an economics or business course at high school and whether they were banked found a statistically significant association between level of high school financial education and being banked (Wiley). https://onlinelibrary.wiley.com/doi/pdf/10.1111/j.1745-6606.2010.01171.x

Financial Literacy Courses in School are Necessary

A mere 31% of young Americans thought that their high school education adequately taught them good financial habits (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

40.2% of those with low levels of financial literacy relied on parents, friends, and acquaintances as their most important source of financial knowledge, compared to 20.8% of those with the highest levels of financial literacy (National Bureau of Economic Research). http://www.nber.org/papers/w13565.pdf

“The number one problem in today’s generation and economy is the lack of financial literacy.” – Alan Greenspan, former Chairman of the Federal Reserve

“Financial literacy is an issue that should command our attention because many Americans are not adequately organizing finances for their education, healthcare and retirement.” – Ron Lewis, former United States Representative

“The single biggest difference between financial success and financial failure is how well you manage your money. It’s simple: to master money, you must manage money.” – T. Harv Eker, author of Secrets of the Millionaire Mind

Graduates Need Financial Education

37% of recent college graduates have been late with a student loan payment at least once in the past year (US Financial Capability). http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

15% of adults roll over $2,500 or more in credit card debt each month (National Foundation of Credit Counseling). https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

Only one in five (19%) say they are not knowledgeable about annuity products in retirement (1 or 2 on a 7-point scale), suggesting many overestimate their knowledge of annuities (The American College). http://retirement.theamericancollege.edu/sites/retirement/files/2017_Retirement_Income_Literacy_Report.pdf

6% of Americans between ages 18-26 are not optimistic about their financial future (Bank of America). https://bankofamerica.com

31% agree they have more debt than the average person (Money Confident Kids). http://www.moneyconfidentkids.com/content/dam/money-confident-kids/PDFs/PKM-Surveys/2017_PKM_Results.pdf

Necessary Elements of School Financial Literacy Programs

Individuals set on incorporating financial literacy into the public education system must always be aware that only quality financial literacy resources for teachers have the potential to induce behavior molding. Concerned community citizens can ensure that the program they are bringing into their schools is of the highest quality by either partnering with a government agency or financial education company, or following the guidelines established by these organizations. The divergence in behaviors of financial literate and illiterate individuals is the difference between a financially secure future and a future plagued by financial struggles.

The Financial Consumer Agency of Canada (FCAC) stresses that tailoring programs toward individual learner needs and the use of interactive activities is critical in capturing the attention of participants and promoting positive behavioral change (Financial Consumer Agency of Canada). https://www.canada.ca

The International Organization of Securities Commissions asserts that partnering with relevant industry experts and education providers to develop and deliver content allows programs to maximize limited resources and leverage one another’s strengths (International Organization of Securities Commissions). https://www.iosco.org/library/pubdocs/pdf/IOSCOPD441.pdf

School Financial Literacy Courses Will Reach All Kids

One reason why we need to teach financial literacy in school is to ensure that every child has equitable access to a fundamental life skill that is related to the financial outcomes of their lives. Separating a financial literacy initiative from school runs the risk of educating only a portion of the community in financial literacy, while leaving the rest without the necessary skills to succeed financially in life. From a more general perspective, why we need to teach financial literacy in school is to produce pupils well-versed in financial matters and ready to overcome any financial obstacles that they may encounter.