Why Money Management Should Be Taught in Schools

Before backing a financial literacy program, people in charge of public policy need to ask themselves why money management should be taught in schools. When they look at recent research, they will find that school is the optimum time to learn these invaluable skills. Recent money management surveys show when students learn the principles of personal finance just when they are beginning to handle their own money, they tend to put their newfound financial literacy into practice and use it for the rest of their lives. The question of why money management should be taught in schools should be replaced by how to implement the most effective money management programs into the curriculum of all schools.

Reasons to Teach Money Management in School

A few of the reasons why money management should be taught in schools are to inform students of the different investment vehicles available to them, the pros and cons associated with each, and how to navigate an increasingly complex financial system. The answer to why money management should be taught in school as opposed to other avenues is to equip students with the framework for prudent investing early on, so as to avoid the need to cleanse bad habits during mid-career when half the time to invest has gone. Providing quality training and information on money management in school sis needed to modify existing money habits.

Learning Money Management in School has a Big Impact on Life

The states of Georgia, Idaho, and Texas began mandating financial education starting in 2000. The improvement in credit scores after going through the program for each of these states is compared against the improvement in credit scores to a nearby state without state-mandated financial education. The credit scores are recorded on a 280-850 scale. For students participating in the programs’ 3rd year of implementation, credit scores increased 10.89 in Georgia, 16.19 in Idaho, and 31.71 in Texas (Financial Industry Regulatory Authority).

http:// www.finra.org /sites/default/files/investoreducationfoundation.pdf

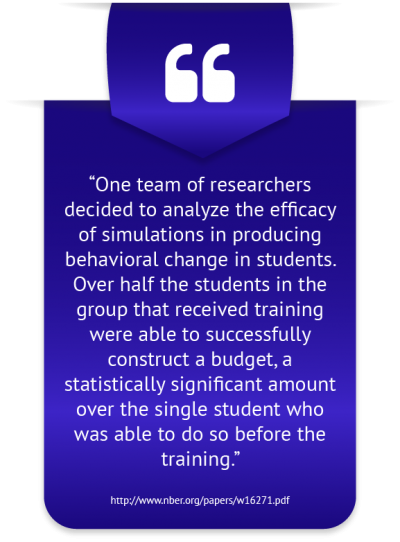

A team of researchers surveyed students at 15 geographically diverse colleges to assess financial knowledge and behavior. Student responses were organized into 1 of 6 categories based on the type of financial education policy a student’s home state had for high school. The categories ranged from a state with no standards at all to states that required a financial literacy course and assessment in high school.

Students whose home states required financial education courses were found to be more likely to save, less likely to make late credit card payments, and more likely to take on a healthy amount of financial risk. While 1.3% of those with no state standards ‘maxed out’ their credit cards, only 0.7% of those with a required course and corresponding assessment ‘maxed out’ their credit cards. When asked if used a budget, 46.7% of those with no state standards replied yes while 52.9% of those with a course and assessment replied yes (National Endowment for Financial Education). https://www.nefe.org/Portals/0/WhatWeProvide/PrimaryResearch/PDF/Gutter_FinMgtPracticesofCollege

Students_Final.pdf

Money Management is Presently Learned from Community, Not in School

A mere 31% of young Americans thought that their high school education adequately taught them good financial habits (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

Researchers at NBER demonstrated the positive relation between the average stock market participation between the individual’s community and the individual’s participation rate in the markets. This effect was proven to be stronger in more sociable communities (National Bureau of Economic Research). http://www.nber.org/papers/w13168.pdf

Lack of Money Management Training is Obvious in Adults

Two in five U.S. adults report keeping a budget and tracking their spending (National Foundation for Credit Counseling). https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

37% of recent college graduates have been late with a student loan payment at least once in the past year (US Financial Capability). http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

58% of 18-26 year olds set aside a portion of their income as savings (Bank of America). https://bankofamerica.com

Almost 50% of millennials don’t believe they could come up with $2,000 within the next month if an emergency arose (PwC). https://www.pwc.com/us/en/about-us/corporate-responsibility/assets/pwc-millennials-and-financial-literacy.pdf

42% of millennials took out an alternative financial service (PwC). https://www.pwc.com/us/en/about-us/corporate-responsibility/assets/pwc-millennials-and-financial-literacy.pdf

“Being promoted to a top position in your organization, or even being elected to public office, does not suddenly endow you with financial literacy, if you did not acquire and develop it, earlier in your life.” – Strive Masiyiwa, founder of Econet Wireless

“Many entrepreneurs struggle to understand payroll taxes, health care and other thorny issues… In other words, they don’t have the financial literacy to scale their businesses and attract investors.” – Daymond John, CEO of FUBU and Sharktank host

“The single biggest difference between financial success and financial failure is how well you manage your money. It’s simple: to master money, you must manage money.” – T. Harv Eker, author of Secrets of the Millionaire Mind

Quality Money Management in School Curriculum

Poor money management skills are far too pervasive among the nation. Millions of students and people in the workforce are making the wrong financial decisions, which are difficult to correct at best and outright impossible to recover from at worse. Preventing individuals from making decisions that can wreak havoc on their financial lives begins with the delivery of quality financial education. Financial literacy changes the habits of learners in a manner conducive to long term financial health.

The President’s Advisory Council on Financial Capability claims that rigorously evaluated pilot programs can help keep costs down while determining which implementation of a program will produce the intended effect (US Dept of Treasury). https://www.treasury.gov/resource-center/financial-education/Documents/PACFCYA%20Final%20Report%20June%202015.pdf

The Federal Reserve Bank of Philadelphia found that there was no statistically significant evidence to suggest that face-to-face counseling prompted greater adoption of healthy financial practices than counseling delivered via technology. Programs that are limited on funds can use technology as a means to reach more people with the same level of efficacy and with lower expenses (Federal Reserve Bank of Philadelphia). https://www.phil.frb.org

Advantages of Learning how to Manage Your Money in School

When wondering why money management should be taught in schools, policy makers should keep in mind that early lessons in money management mean that students will have more time to practice those sensible strategies in order to grow their assets. They should also remember that poor habits will not have to be cleansed and replaced with a healthier framework for analyzing investment choices and managing household finances. To change behaviors takes more than just proving a few money management games or handing out a few money management worksheets – it takes longer focus that traditional subjects enjoy. Giving our youth the best possible chance to succeed is why money management should be taught in schools.