Personal Finance Case Studies

While basic financial knowledge must be initially provided in any successful financial education program, personal finance case studies have a lot to offer financial education curriculums as well. With many young Americans experiencing tough financial issues and concerned about their financial states, exposure to real-life examples of personal financial situations has been proven to not only assuage fears but also contribute to measurable improvement in handling personal finances. Taught as part of a thorough curriculum, these case studies are proven to drastically improve the financial literacy of students.

How Personal Finance Case Studies Work

Personal finance case studies relate content taught in class to real-world situations. By presenting personal finance issues in context, these case studies assist educators by exposing learners to situations that they might experience themselves. Students have the opportunity to learn from errors discussed in the case studies, critically considering the steps they will take to avoid financial illiteracy or falling into similar situations in their futures.

The Real-Life Situations Molding Youth Financial Behaviors Today

A statistically significant association was determined between negative financial habits, such as gambling among Australian youth, and the influence of peers and parents. https://www.sciencedirect.com/science/article/pii/S0140197103000137?via%3Dihub

In a survey by OECD, well over a quarter of respondents replied that their culture influenced their attitudes toward wealth. https://www.oecd.org/finance/financial-education/2017%20Seminar%20on%20financial%20education %20and%20financial%20consumer%20protection%20LAC%20Wood%20.pdf

6% of Americans between ages 18-26 are not optimistic about their financial future. https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

54% of millennials expressed worry that they would not be able to pay back student loans. https://www.pwc.com/us/en/about-us/corporate-responsibility/assets/pwc-millennials-and-Financial-literacy.pdf

The Personal Impact Of Financial Illiteracy

Households that scored higher on a specially constructed savings index were found to be more likely to own a checking account and have an emergency fund. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

In a survey conducted by the National Financial Educators Council, 5.2% reported they had been turned down from a job due to a lack of financial knowledge, and 18.2% responded they were not sure. https://www.financialeducatorscouncil.org/financial-literacy-statistics/

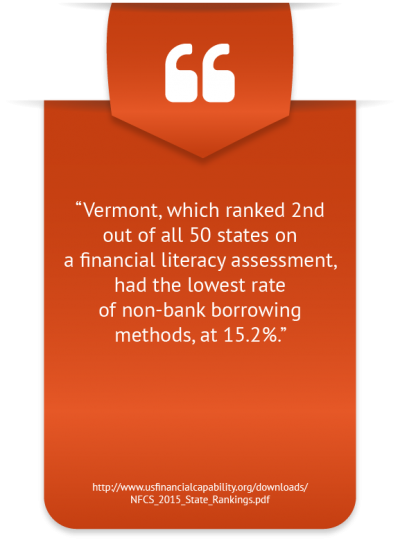

North Dakota, which ranked 4th out of all 50 states on a financial literacy assessment, had the highest percentage of respondents at 55.5% declare they had an emergency fund. http://www.usfinancialcapability.org/downloads/NFCS_2015_State_Rankings.pdf

The Positive Impact of Personal Finance Case Studies

Students who underwent the Moneytalks educational curriculum demonstrated positive behavioral changes. A “saving scale” constructed by the author was the composite of a series of questions asking students about their savings habits. The mean value of the savings scale rose from a mean of 24.28 to 26,78, which was deemed statistically significant. Furthermore, statistically significant differences were noted for the proportion of kids who would compare price and buy on sale. http://ucanr.edu/sites/consumereconomics/files/136495.pdf

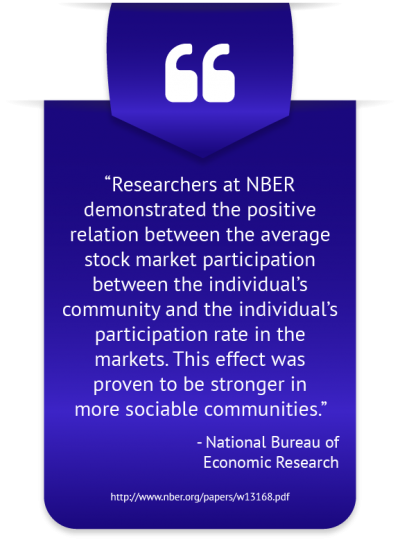

Low-income workers attending an employer-sponsored financial education program were 11.5% more likely to participate in 401(k) plans and save more for retirement than peers who elected not to attend the education initiative. http://www.nber.org/papers/w5655.pdf

The President’s Advisory Council on Financial Capability approved 4 key themes that a successful program should focus on. The first requires financial materials to be readily accessible and affordable for members of the community. https://www.treasury.gov/resource-center/financial-education/Documents/PACFCYA%20Final%20Report%20June%202015.pdf

The International Organization of Securities Commissions provides 7 practices that have been identified as integral to success for a financial literacy initiative. The first practice calls for a curriculum designed to impart basic investment competencies and awareness of various investment products. https://www.iosco.org

The Need for Inclusion of Personal Finance Case Studies In Curriculum

With recent academic literature suggesting that learners exhibit greater retention when material inside the classroom is connected to their lives, there is a cogent argument to be made that personal finance case studies belong in effective personal finance lesson plans. While personal finance case studies are an effective tool, participants must first be equipped with some financial knowledge in order to discern the mistakes the individual in the case study made and learn from those mistakes.

[1] National Financial Educators Council, Personal Finance Facts [2] National Financial Educators Council, How to Start a Personal Finance Business