Need for Financial Literacy

With more research highlighting the consequences of not knowing how to manage personal finances, the need for financial literacy is becoming glaringly obvious. The right people are beginning to take notice and act, but more needs to be done. The faster public awareness spreads, the more people will speak out, causing the financial literacy movement to finally take hold. When policy makers and educators realize the critical importance of financial education and fully understand the need for financial literacy, programs and initiatives will pop up everywhere and we will become a nation of financially savvy individuals.

The Obvious Lack of Financial Literacy

The need for financial literacy is evidenced by the poor financial situation of individuals: drowning in debt without a budget plan and making misguided decisions about their money. Most of these poor financial behaviors stem from financial illiteracy (basic lack of understanding of financial competencies). These problems illustrate the need for financial literacy programs that help participants gain the information necessary to make prudent choices about their finances. Equipped with financial literacy, individuals can make healthy decisions about their money that will lead to a more stable financial life.

Basic Financial Literacy Makes a Big Difference

The Federal Deposit Corporation (FDIC) analyzed the intermediate-term impact of a financial literacy program on consumers’ behavior and confidence 6 – 12 months after the end of the program. They found that consumers were more likely to have a checking account, budget wisely, save for retirement, and more. After the program, 78% of respondents reported they had a checking account, up from 12% before they had undergone the program. Another 69% reported their level of savings had increased after taking the program, with only 3% reporting that it had declined (Federal Deposit Insurance Corporation). https://www.fdic.gov/consumers/consumer/moneysmart/pubs/ms070424.pdf

The states of Georgia, Idaho, and Texas began mandating financial education starting in 2000. The improvement in credit scores after going through the program for each of these states is compared against the improvement in credit scores to a nearby state without state-mandated financial education. The credit scores are recorded on a 280-850 scale. For students participating in the programs’ 3rd year of implementation, credit scores increased 10.89 in Georgia, 16.19 in Idaho, and 31.71 in Texas (Financial Industry Regulatory Authority). http:// www.finra.org /sites/default/files/investoreducationfoundation.pdf

Parents and Schools Need to Teach Financial Literacy

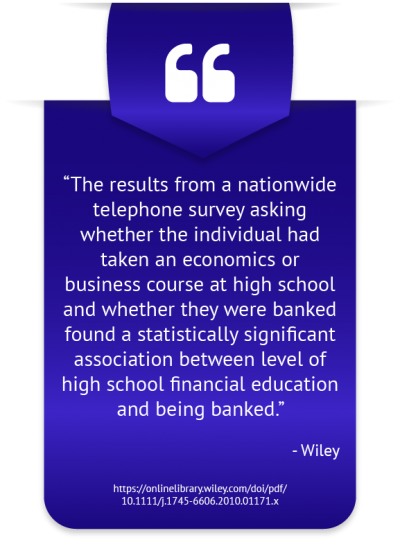

A research study analyzing the effects of parents’ values on children found a statistically significant positive association between parent’s savings rates and children’s savings rates (University of Agder). https://home.uia.no/ellenkn/WebleyNyhus2006.pdf

A mere 31% of young Americans thought that their high school education adequately taught them good financial habits (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

37% of recent college graduates have been late with a student loan payment at least once in the past year (US Financial Capability). http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

Two in five U.S. adults report keeping a budget and tracking their spending (National Foundation for Credit Counseling). https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

58% of 18-26-year-olds set aside a portion of their income as savings (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

What Experts Think About the Need for Financial Literacy

81% of college educated millennials have at least 1 long standing debt (PwC). https://www.pwc.com/us/en/about-us/corporate-responsibility/assets/pwc-millennials-and-financial-literacy.pdf

6% of Americans between ages 18-26 are not optimistic about their financial future (Bank of America). https://bankofamerica.com

“Financial literacy is not an end in itself, but a step-by-step process. It begins in childhood and continues throughout a person’s life all the way to retirement. Instilling the financial-literacy message in children is especially important, because they will carry it for the rest of their lives.” – George Karl, former NBA coach

“We need to have financial literacy in America, not just complaining about obstructionism. We need solutions.” – Kabir Sehgal, bestselling author of 8 books

“It’s pretty much how we get anything added to the curriculum. When parents said children needed to be computer literate, the schools started responding. The same thing is true of basic financial literacy.” – Elizabeth Warren, United States Senator

Financial Literacy Programs Need Proper Design

The behavior-molding we cite below shows what is possible when financial literacy is done properly. People who have a solid knowledge of financial matters are able to more accurately discern different financial decisions and make the right choices aligned with their long-term goals. Individuals who are just entering the workforce and have not thought about the end of their career, for example, may realize the importance of saving for retirement early and open a 401(k) plan. A poorly made program will be one that may improve knowledge, but does not prompt any behavioral change.

The President’s Advisory Council on Financial Capability urges financial programs to leverage technology in order to educate a generation that actively utilizes technology to learn. Teachers can incorporate games and apps into the classroom to facilitate learning and engage students (Department of the Treasury). https://www.treasury.gov/resource-center/financial-education/Documents/PACFCYA%20Final%20Report%20June%202015.pdf

The Federal Reserve Board’s Division of Consumer and Community Affairs stresses that delivery of information must be presented at an opportune time, when consumers are most likely to retain information. First-time home buyers would be receptive to pre-purchase counseling, for example (Federal Reserve). https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

The Dire Need for Financial Literacy is Being Answered

With so many real-life examples highlighting the negative consequences of poor money management, the need for financial literacy has never been more obvious. Financial competency means individuals will have the skill set necessary to manage their finances so as to alleviate stress, build a bigger nest egg for retirement, and budget appropriately according to their income. The critical need for financial literacy has spurred public policy makers to take steps in outlining a national strategy for financial education. Further, it has led to the proliferation of financial education initiatives designed to impart financial knowledge to participants.