History of Financial Inclusion

The history of financial inclusion around the world shows that progress has been a long and ever-evolving journey to connect every individual to basic financial services. Beginning in the late 1990’s and early 2000’s many organizations began to shift from offering solely microcredit services to also offering basic access to financial services such as savings and insurance. Non-governmental organizations (NGOs) began to obtain licenses to accept deposited savings and offered an array of other financial services to lower income individuals, often in third world countries.

Modern Financial Inclusion is a Two-Fold Challenge

If the push for bringing financial institutions to low income communities is hard, there is another challenge that financial education providers face in facilitating financial inclusion. Low income individuals with no financial literacy education – and often little to no education beyond primary schooling – must be equipped with the knowledge to use these basic financial services. The main focus of educators, who have found that education is not overly difficult, is to induce behavioral modification and to make financial inclusion a fundamental part of the lives of low-income individuals.

Expansion of Financial Inclusion

Despite the increased efforts of global organizations to bring basic financial services to the 2 billion people without so much as a bank account, only an estimated 10% have been reached by the microfinance industry. To increase the efficacy of the fight for financial inclusion, partnerships between government agencies, microfinance institutions, and global corporations have been drawn up. Digital finance innovations have also been identified as harboring the potential to penetrate remote communities with no access to rudimentary financial services.

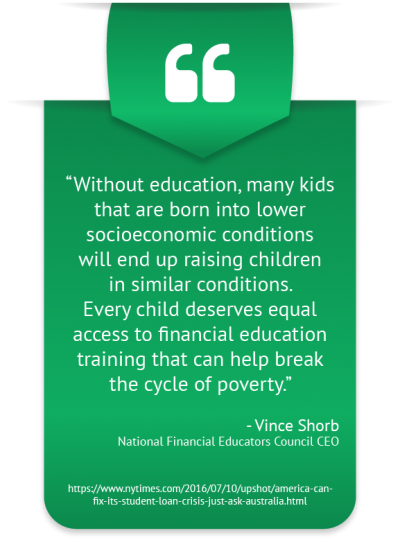

Experts Speak Out About Financial Inclusion

Experts Speak Out About Financial Inclusion

“Being promoted to a top position in your organization, or even being elected to public office, does not suddenly endow you with financial literacy, if you did not acquire and develop it earlier in your life.” – Strive Masiyiwa, founder of Econet Wireless

“The number one problem in today’s generation and economy is the lack of financial literacy.” – Alan Greenspan, former Chairman of the Federal Reserve

“I think people don’t understand compound interest because typically no one ever explains it to them and the level of financial literacy in the US is very low.” – James Surowiecki, journalist at The New Yorker and author of “The Financial Page” column

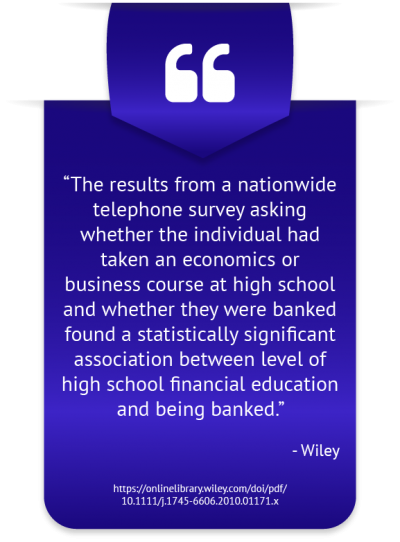

Financial Inclusion is Harmful Without Financial Literacy

Financial Inclusion is Harmful Without Financial Literacy

The average debt of students when they graduated from college rose from $18,550 (in 2004) to $28,950 (in 2014), an increase of 56 percent (Institute for College Access and Success). https://ticas.org/sites/default/files/pub_files/student_debt_and_the_class_of_2014_nr_0.pdf

Almost 50% of millennials don’t believe they could come up with $2,000 within the next month if an emergency arose (PwC). https://www.pwc.com/us/en/about-us/corporate-responsibility/assets/pwc-millennials-and-financial-literacy.pdf

History Shows That Financial Inclusion and Education Lead to Personal Empowerment

Worldwide financial inclusion data is clear that getting more people into a more advanced financial system may be a worthy goal but it cannot be considered alone. The lofty goal of inclusion must become intimately tied to financial literacy. Young adults in the US have recently shown that financial inclusion without prior financial literacy is a recipe for lifetime disaster with the potential to continue throughout generations. When the numbers are studied closely, this phenomenon will become obvious throughout the history of financial conclusion. People need to first understand the concepts and skills of financial prudence and planning for the future, before they are included in a modern banking system. When people are first educated on personal financial management and are then allowed within modern financial systems, the potential for an empowered, fulfilling life improves dramatically.

[1] National Financial Educators Council, ‘Financial Inclusion Definition’

[2] National Financial Educators Council, ‘Financial Inclusion Quotes’

[3] National Financial Educators Council, ‘Financial Wellness Quotes’