Financial Education Statistics

Statistics about the current state of financial education shine light on many important issues having to do with the lack of monetary literacy we face as a nation. They also point out the dramatic consequences of inaction, highlight the best solutions to the problem and show us a clear path forward. These solutions lie in changing our views of talking about money. Financial education statistics show that by being more open about finances, parents, educators and those involved in public policy can have a positive impact on individuals who would otherwise never be exposed to the idea of taking responsibility for their personal finances.

Financial Education Problems and Solutions

Financial education statistics highlight the severe lack of financial knowledge and subsequent discontent that afflicts millions of individuals who were not able to receive a basic education in financial literacy. The same statistics that indicate a dire need for improved financial education also attest to the efficacy of well-crafted financial literacy initiatives based on data and industry wide best practices. Recent financial education statistics clearly demonstrate that efforts to educate individuals, both young and old, in financial literacy result in improved financial behavior.

Financial Behavior is Copied from Peers and Learned Through Education

In a survey by OECD, well over a quarter of respondents replied that their culture influenced their attitudes toward wealth (Organization for Economic Cooperation and Development). https://www.oecd.org/finance/financial-education/2017%20Seminar%20on%20financial%20education

%20and%20financial%20consumer%20protection%20LAC%20Wood%20.pdf

Parents who have three or more types of savings are more likely to have kids who discuss money with them (83% vs. 66%) and less likely to have kids who spend money as soon as they get it (40% vs. 52%) or lie about their spending (34% vs. 43%) (Money Confident Kids). http://www.moneyconfidentkids.com/content/dam/money-confident-kids/PDFs/PKM-Surveys/2017_PKM_Results.pdf

A survey of 15-year-olds in the United States found that 18 percent of respondents did not learn fundamental financial skills that are often applied in everyday situations, such as building a simple budget, comparison shopping, and understanding an invoice (Organization for Economic Cooperation and Development). http://www.oecd.org/education/Education-at-a-Glance-2014.pdf

Financial Education Occurs at School and at Home

Less than one in ten (7%) understand that small company stock funds have a higher return over time than large company stock funds, dividend paying stock funds, or high yield bond funds (The American College). http://retirement.theamericancollege.edu/sites/retirement/files/2017_Retirement_Income_Literacy_Report.pdf

Vermont, which ranked 2nd out of all 50 states on a financial literacy assessment, had the lowest rate of non-bank borrowing methods, at 15.2% (US Financial Capability). http://www.usfinancialcapability.org/downloads/NFCS_2015_State_Rankings.pdf

46% of Americans say they have set aside 3 months-worth of living expenses in the case of an emergency (US Financial Capability). http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

Households that scored higher on a specially constructed savings index were found to be more likely to own a checking account and have an emergency fund (Federal Reserve). https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

Financial Literacy Education Improves Financial Planning

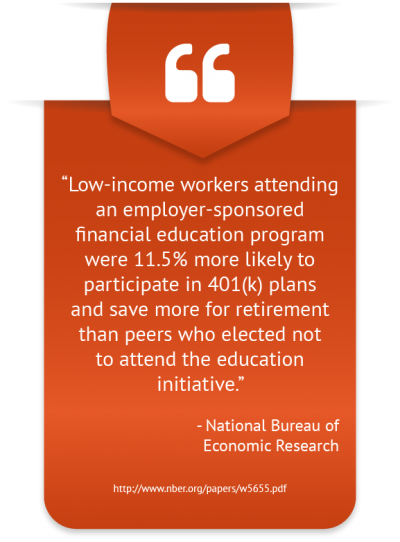

Low-income workers attending an employer-sponsored financial education program were 11.5% more likely to participate in 401(k) plans and save more for retirement than peers who elected not to attend the education initiative (National Bureau of Economic Research). http://www.nber.org/papers/w5655.pdf

Researchers take advantage of a survey recording self-reported savings rates, as measured by amount of unspent take-home pay along with voluntary deferrals (e.g. 401(k) plan), and the state the respondent went to high school in. This is used to determine whether state mandated financial education curricula have an impact on the amount individuals save. Those entering high school five years after the implementation of the mandate had a savings rate of 1.5 percentage points higher than for students not exposed to a mandate (National Bureau of Economic Research). http://www.nber.org/papers/w6085.pdf

The Citi foundation proposes that programs should revolve around actual financial products that participants can then implement to make smarter financial choices. Information gleaned from research, pilot programs, and other evaluations should be shared other stakeholders in the field so as to maximize efficiency (Citigroup). https://www.citigroup.com

The Jump$tart Coalition prescribes that materials are specifically tailored toward the intended target group. Lesson plans are kept up to date and regularly revised to be accurate and relevant (Jumpstart). https://www.jumpstart.org

Conclusion

Financial education statistics, while often discouraging, should not dissuade educators from creating well designed financial literacy programs. Rather, current financial education statistics should serve as a reminder to the pervasiveness of the financial illiteracy epidemic and compel both public and private organizations to bolster their financial education efforts. Through coordinated efforts and by utilizing sustainable program best practices, initiatives have the ability to transform financial behavior and improve the financial education statistics years from now.