Youth Money Management Lessons: Where to Begin

Interested in creating a youth money management program, but don’t know where to start? You’ve reached a good launching point to get financial literacy programs for youth off the ground. This website is designed to support people who want to deliver youth money management instruction by presenting topics of value and discussing the financial obstacles kids must tackle.

Valuable Subject Matter for Teens

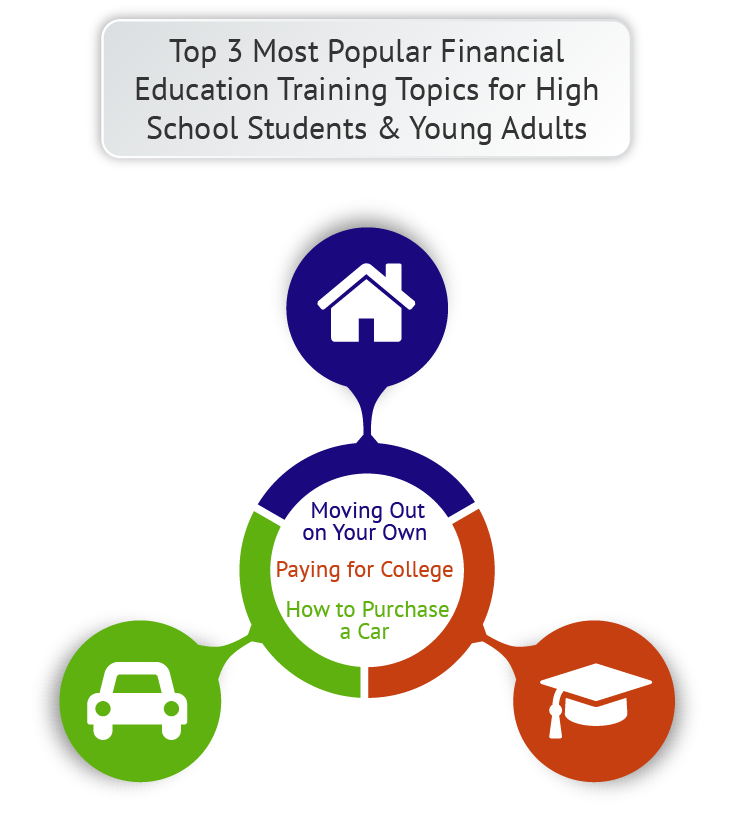

Teens will receive greatest benefit from youth money management lessons that address the topics that are unique to young adults’ decision-making. Three cases in point include vehicle purchasing, educational funding, and independent living.

Buying a vehicle involves a series of money management practices: setting objectives; budgeting for the car (including all expenses of ownership, beyond just the loan payment); qualifying for a loan; obtaining credit; and choosing an appropriate insurance policy. Workshops that address these subjects will attract young participants who are eager to learn.

How to pay for university is a second key topic for teenagers. Such a seminar might guide youth through the processes of selecting career options, calculating educational ROI, developing a college budget, and various funding streams such as student loans, grants, and scholarships.

Lastly, independent living represents an important subject that many young people will be interested to study in a personal finance class for high school levels. By “independent living,” we mean gaining the knowledge and skill to set personal finance goals, create a budget, rent or buy a house/apartment, and categorize all the expenses of independent life (rent, transportation, insurance, food, utilities, etc.).

Features that will Influence Youth Money Management in the Future

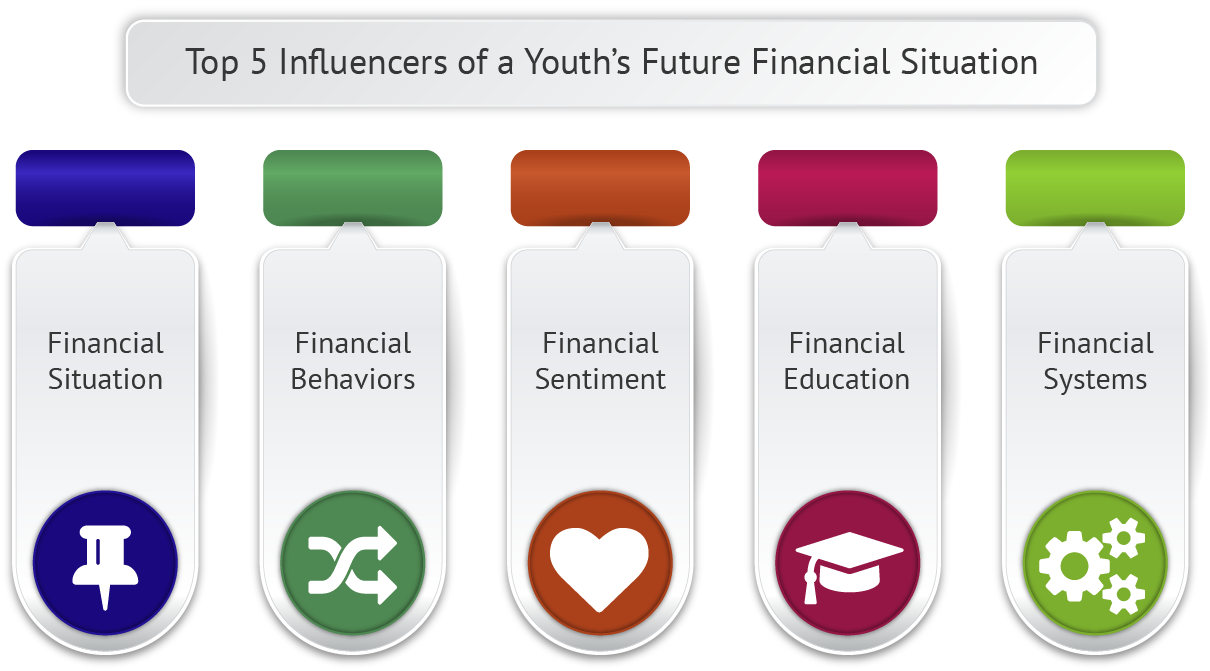

Five essential features will influence teens to adopt certain youth money management habits: their family situations, behavior patterns, money sentiments, financial education exposure, and money management systems. Financial literacy for youth programming should address all those issues.

Financial Situation: this term refers to the socioeconomic conditions into which a child is born. What is the parents’ SES level? How good are they at managing their finances? What are the child’s opportunities for upward mobility?

Financial Behavior Development: youth money management behaviors start emerging when the kids are very young. Lots of factors affect their habits including advertising exposure, peer influences, parental modeling, and the environmental conditions.

Financial Sentiment: this phrase defines the feelings and emotions people have toward money. In youth money management, kids’ financial futures will depend on the attitudes and beliefs they start forming in childhood and carry forward into adulthood. This sentiment includes how capable they believe they are at managing their funds. Emotions should be a fundamental component of financial literacy classes in high school and college.

Financial Education: how much exposure youth have to solid money management education makes a huge difference in their personal finance futures. Yet very few schools and parents are preparing teens for an independent existence.

Money Management Systems: this term expresses the support and structures youth need to set themselves up for financial success. In other words, they need bank accounts, retirement savings, and tracking schedules in place to guide their personal finance decision-making.

Check out this page from You4Youth, sponsored by the US Department of Education, for more resources: You For Youth // Financial Literacy for All (ed.gov).

Who Teaches our Youth Money Management?

Every year our institutes of higher education turn out a new crop of college graduates embarking on life’s journey. Yet research has shown that these young adults are dangerously unprepared for the financial realities life is likely to throw their way. Among American youth, money management skills are scarce. Public high schools do not provide practical financial education, and many parents are uncomfortable broaching the topic with their children.

Given this lack of education in money management for teens, young college graduates are likely to make mistakes. And even the smallest mistake can have devastating, long-lasting negative consequences. For example, a single late payment on a credit card can ruin one’s credit score for 7 years into the future. During that time, the individual will only qualify for astronomical interest rates on auto, home, credit card, or personal loans—if they qualify for any loans at all.

Here’s another reason why we need financial literacy programs for youth. Extended life spans and the retiring Baby Boom generation have led analysts to predict that, by the time your teens and college-aged youth are ready to retire, Social Security will be a distant memory. And if you assume your child will be able to retire on a corporate pension, think again. More and more companies are scaling back or even eliminating pension programs.

So who should teach our kids money management? In a 2012-13 online poll by the National Financial Educators Council (NFEC), 65% of the 622 participants said “parents” were responsible for teaching kids about money. And the fact that schools lack funding and support for teaching financial literacy just lends credence to that belief. But sadly many parents feel unqualified or uncomfortable teaching their teens about money. That’s where the NFEC comes in. The organization provides free resources, consultation, and products to support parents interested in youth money management programming, regardless of their own personal finance skills.