What is Financial Literacy?

To answer the important question, “What is financial literacy,” let’s define each word individually. The word finance applies to “any dealings with money.” Then, literacy refers to “knowledge or competence.” Therefore, when put together Financial Literacy means, “Knowledge and competence of how to deal with money.” When people are financial literate, they understand financial topics. However, this does not mean they will make right decisions when it comes to managing their money. Driven by sentiment and systems, their financial behaviors play an important role in their overall financial outcomes.

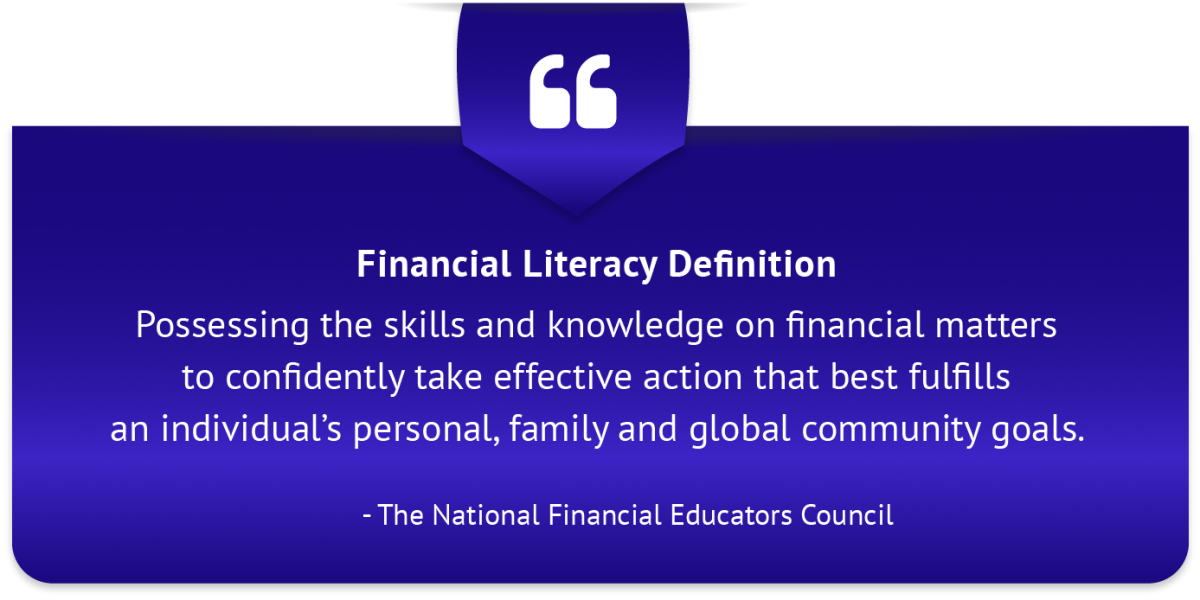

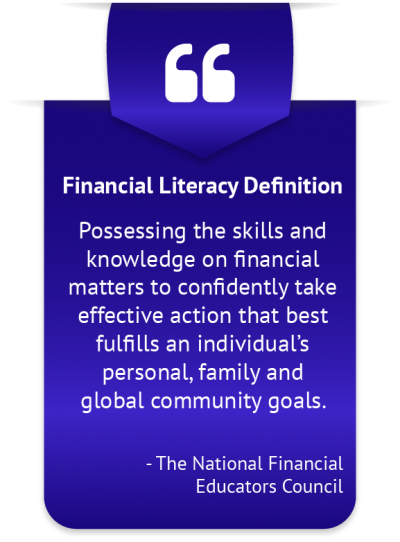

Financial Literacy Definition

The financial literacy definition developed by the National Financial Educators Council:

Possessing the skills and knowledge on financial matters to confidently take effective action that best fulfills an individual’s personal, family and global community goals.

Definitions of Financial Literacy

“Financial literacy is a combination of financial knowledge, skills, attitudes and behaviors necessary to make sound financial decisions, based on personal circumstances, to improve financial wellbeing” (Australian Securities and Investments Commission). https://files.MoneySmart.gov.au

“Personal finance describes the principles and methods that individuals use to acquire and manage income and assets. Financial literacy is the ability to use knowledge and skills to manage one’s financial resources effectively for lifetime financial security. Financial literacy is not an absolute state; it is a continuum of abilities that is subject to variables such as age, family, culture, and residence. Financial literacy refers to an evolving state of competency that enables each individual to respond effectively to ever-changing personal and economic circumstances. The combination of knowledge, skills, attitudes and ultimately behaviors that translate into sound financial decisions and appropriate use of financial services.” – The Center for Financial Inclusion

“A level of financial knowledge and skills that enables individuals to identify the fundamental financial information required to make their conscious and prudent decisions; and after the acquisition of identified data allows them to interpret said data, make decisions on their basis, all the while assessing potential future financial and other consequences of their decisions.” (National Bank of Hungary, 2008).

“The ability to use knowledge and skills to manage one’s financial resources effectively for lifetime financial security”.

https://www.jumpstart.org

Aspects of a Good Financial Literacy Program

Modification of financial behaviors is the result of proper financial literacy education efforts. Education in personal finance must adopt well-researched delivery methods and program practices in order to maximize the potential for positive behavior molding of students. Multiple papers have shown personal finance knowledge to be associated with positive financial habits that support the long-term financial goals of an individual. Those looking to implement financial education within their communities should be aware that only when done right can the benefits of financial literacy be recognized.

A study undertaken in the Dominican Republic compared two distinct approaches to financial literacy: a standard accounting curriculum and a rule-of-thumb training that taught financial heuristics and found that the simpler rule-of-thumb training produced a larger effect in firms’ financial practices and made them more likely to keep accounting records, forecast monthly revenues and objectively report financial figures (Poverty Action Lab). https://www.povertyactionlab.org

The Financial Literacy and Education Commission (FLEC) states that building public awareness of educational resources is the first step a program should take to ensure that its carefully crafted materials are implemented in communities (Financial Literacy and Education Commission). https://www.treasury.gov/

Forming the Habits of Financial Literacy

A research study analyzing the effects of parents’ values on children found a statistically significant positive association between parent’s savings rates and children’s savings rates (Journal of Economic Psychology). https://home.uia.no

An additional year of schooling increases the probability of having an investment income by 4.4% for whites and 1.7% for blacks (Harvard Business School). http://www.people.hbs.edu

Financial Literacy is Best Learned in Youth

Two in five U.S. adults report keeping a budget and tracking their spending (National Foundation for Credit Counseling). https://www.nfcc.org

65% of adults in the United States report using a saving account (National Foundation for Credit Counseling). https://www.nfcc.org

Nearly two in ten adults roll over $2,500 or more in credit card debt each month (National Foundation for Credit Counseling). https://www.nfcc.org

Experts Speak on the Importance of Financial Literacy

“Financial literacy is just as important in life as the other basics.” – John W. Rogers, Jr., CEO Ariel Capital Management

“The good news, though, is that all of us can improve the security of our futures through financial literacy. With a better understanding of the basics of finance—how to save, budget and invest—we can increase both our earning potential and our prospects for a solid financial future.” – Reba Dominski, President of U.S. Bank Foundation

What is Financial Literacy and Why Is It Important

A growing realization that our youth are graduating without certain fundamental skills has led concerned individuals to seek out what our education system is missing. Once they find out that our youth are lacking, especially in terms of financial decision making, they ask the question: what is financial literacy? When answering the question of, “What is financial literacy,” it is important to keep in mind that this is a broad topic that deals with the efficient management of one’s personal finances.

A reason why so many people are asking the question of, “What is financial literacy,” is in part due to the understanding of many that financial literacy is a required skill to reach your financial goals. The question, “What is financial literacy,” has broad answers, but at its core, financial literacy involves the use of knowledge to make astute and sustainable financial decisions. In order to teach such a skill to our communities, individuals must advocate for financial literacy programs within our schools.