Guide to Finding the Best Personal Finance Textbooks

Have you been perusing around online in search of personal finance textbooks? Not many reliable options can be found, unfortunately. Now that you’re here, you can stop worrying, because your search has led you to the best place. We have worked hard to develop a complete guide centered on the steps that need to be taken in order to build a high-quality financial education course, in order to help both people and organizations reach their financial potential.

The NFEC offers personal financial literacy textbook online to both people and firms all across the world, which uses totally customizable material for any group of users – no matter how they fit into the world socioeconomically or their age group.

Our well-tested resources are engaging, entertaining, leave a lasting mark – and get a ton of positive feedback.

Personal Finance Textbooks in the Real World

Eve is a supervisor at a call center in a college town and oversees 38 employees who are mostly university students. After a number of them had approached her with questions related to their personal finances, she wanted to provide them with some sort of lessons using personal financial literacy textbook online. The sole issue she needed to deal with was how to get the ball rolling. She had already, throughout her life, become quite knowledgeable on the topic herself, but teaching wasn’t necessarily her strength. That’s why she understood that finding some external teaching assistance would be best if she was to convey this critical information.

After informally speaking with all of her team members, she came to the realization that most of them didn’t even possess a basic level of knowledge on this topic, and that what this group really needed was easy-to-digest material on managing money.

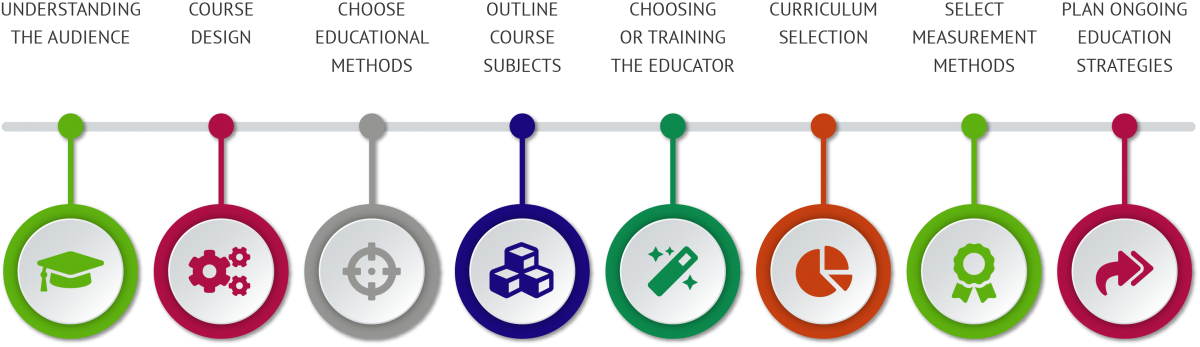

Positioning to Succeed

At the outset, Eve’s idea was to design her own series of workshops that would help this group of people develop an understanding of their finances. She planned on covering the basics quickly, so she intended on starting with the fundamentals. Further down the road, though, her plan was to use interesting personal finance curriculum to increase the entire group’s confidence level in personal finance.

The Personal Finance Textbooks Key

With Eve already decided when it came to her short-term blueprint and future plans for the group, she could start to find the best way to provide them with these critical personal finance textbooks. However, what would determine the pace of the program? What about the delivery of the material? This group, in particular, had a wild assortment of different schedule conflicts and availability. That’s what led her to decide on an internet-based program that could be done on their own time.

Zeroing In: Personal Financial Literacy Textbook Online

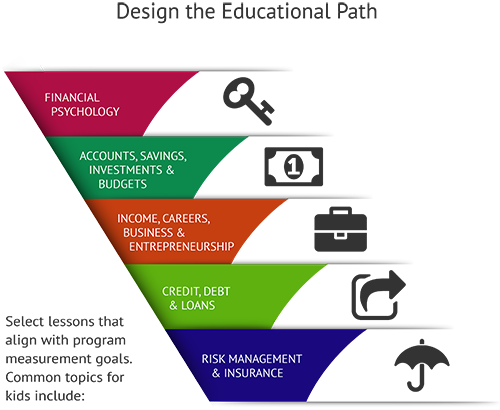

What Eve needed to proceed to next was figuring out a more limited focus for her personal finance lessons. As the entire group was essentially new to this topic, she knew that it would be best to give them a general overview of the topic using broad personal finance textbooks. She also wanted to include a variety of games and a personal finance word whizzle to help the memorize key points in a engaging way.

Getting the Timing Right

What Eve realized she would need was a course option that could address this subject focus while also using engaging, interactive learning activities, and one that would have the possibility of fitting around everyone’s incompatible schedules. With that in mind, she realized that a modular, flexible learning experience would be the best type of program.

Help Finding Personal Finance Textbooks

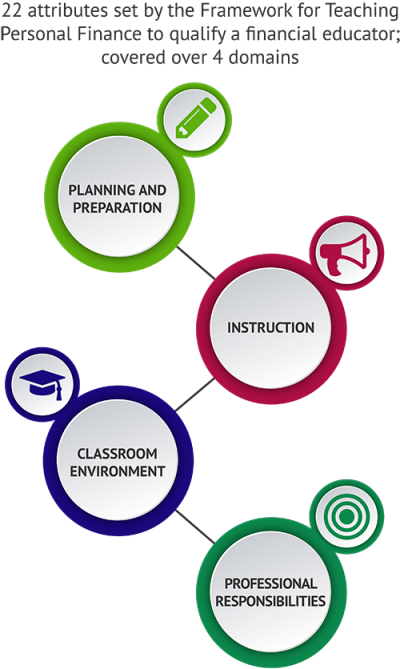

Eve realized that building a course like this, based on a personal finance textbook, would be doable for her, but she became worried that it wouldn’t be sufficiently fun or engaging. In an effort to make sure the course would be impactful enough, she decided to get in contact with a qualified personal finance speaker and get some assistance for the “fun and engaging” aspect. Thanks to some additional help from an experienced professional in the field, she was much more confident.

Setting Out, Following the Roadmap

Out of the 38 call center employees who participated in her course, 36 of them (94%) managed to complete the whole program. Out of all the employees who successfully finished the first overview of personal financial literacy textbook online, all of them (100%) mentioned in a post-course survey that their level of knowledge on personal finance had been “significantly” enhanced. After all was said and done, Eve generated a full report that detailed the participant data from the course – so she could demonstrate how beneficial and helpful the overview of personal finance textbooks had been.

The Ever-Crucial Follow-Up

If this group was to find success in the future, Eve realized that she would need to provide them with ongoing support. Immediately following the end of the first overview of personal finance textbooks, she decided to write out some individual emails to each of them, encouraging their ongoing learning in this field.

To enable each of them to retain what they had picked up in the course, Eve decided to offer them all follow-up sessions on a monthly basis. This would allow them to all continue growing the foundation of important knowledge that they had all began to construct.