A Course on Financial Education for the Poor Will Change Your Life and Theirs

If you feel a pull to teach financial education for the poor, look no further. We offer the resources and support you need to design and build your own course on financial education for low income families. Reading the story below will show you that it’s not an overwhelming project.

The NFEC is an independent organization offering professional resources and support for financial literacy education. Our material does not contain ads and we are free of the ulterior motives of background financial supporters. Financial education is our prime directive.

Making a Difference with Financial Education for Low Income Families

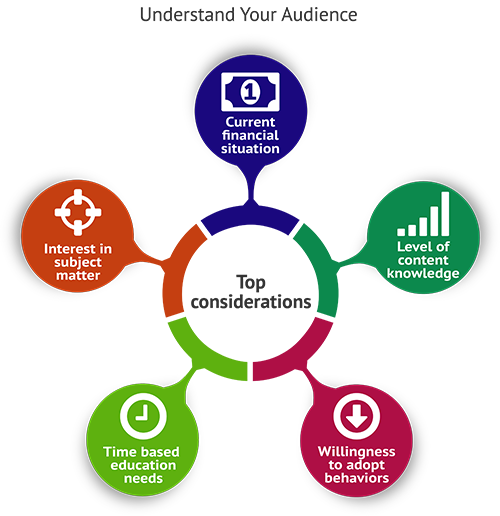

Alex volunteered at a community center. She saw a need for a financial education program for the poor. She started by defining who she wanted the program to reach: people from low-income families, ages 30 thru 50. Her work at the community center provided plenty of evidence that there was an immediate need.

She needed guidelines to figure out how to build such a program. She found exactly what she needed at the NFEC.

Learning Objectives of Teaching Financial Education for Low Income Families

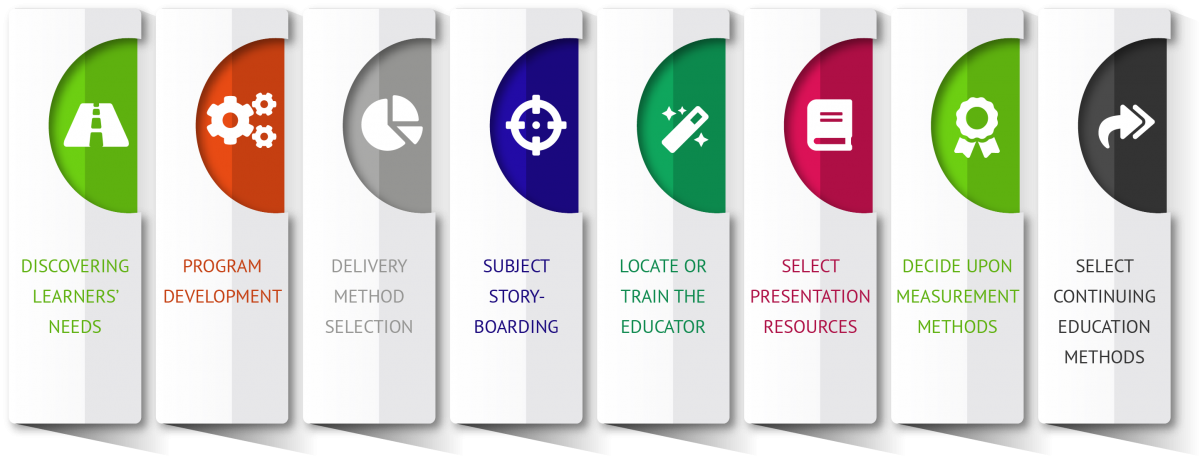

Alex wanted her students to get to a level of knowledge that would enable them to use what they learned in class. This meant getting them to the skills and concepts stage of Webb’s Depth of Knowledge scale. She would push them to reach strategic thinking, but if that was asking too much for this first class, she’d be OK with that. A course with 32 hours of class time would be sufficient to empower them to make positive changes in their financial behavior.

How to Deliver the Course Material to Maximize Financial Education for the Poor

The course would be presented to low-income adults who were old enough to know they had to plan for retirement and young enough that it wasn’t too late. Since this audience might not have a computer and internet, she decided that live instruction at the community center would make the class more accessible than an online program. The pace would be a hybrid system, based on a timeline and achievement. This would enable Alex to keep the class moving while making sure the students were ready to advance to a deeper level of knowledge.

Selecting the Topics to Teach in an Adult Class Addressing Financial Education for the Poor

Curriculum Considerations in Financial Education for Low Income Families

The next step was for Alex to consider the necessary and desired aspects of her financial education curriculum. It had to meet formal educational standards, so the class would be credible. It needed to be flexible and offer modules where students could dive deeper into topics that interested them. It also had to be directly relatable to the real-world situations that these low-income families struggled with every day. Helping poor adults with their immediate financial struggles would keep them engaged and incentivized to learn more.

A Certified Educator to Teach Financial Literacy to Poor Adults and Low-Income Families

Alex’s Course on Financial Education for the Poor is a Success

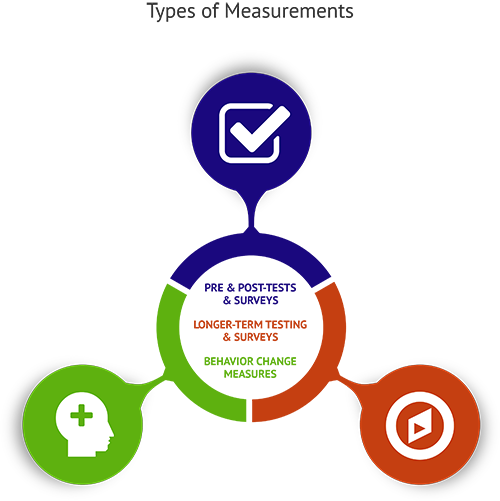

Of the 23 registered students, 19 of them graduated. 82% was a higher completion rate than Alex had anticipated. Those who graduated showed significant improvement in their financial knowledge.

Alex compiled the data into a report showing the undeniable value this program had on the community and the individuals within it. She would make the report the center piece of her application for funding and growth.

Next Steps in Financial Education for Low Income Families

Alex couldn’t just leave her students to fend for themselves with their new knowledge from the basic financial literacy course. She had to provide a supportive environment where they could solidify what they had learned and gain confidence in using it to improve their poor personal financial situations. To this end, she kept the Facebook going and it stayed active well after the course was complete.

She presented participation awards for those that completed the financial literacy program for low income so they could use to increase their incomes by getting better jobs or raises at their current position. She then set her sights on expanding her program to different local areas and offering continuing education.

Alex and her students unanimously agreed that this single course on financial education for the poor had changed their lives. Although not financial education professionals, they did leave the class more confident they can work toward their long-term financial goals.