Hints for Offering Financial Education for Youth

In today’s complex financial environment, many people have become interested in offering financial education for youth. But where should you start? This webpage serves as a good jumping-off point: we provide tips on the best topics to choose in financial literacy programs for youth and adolescents, and describe some of the life events they are likely to be experiencing.

What Subjects Should a Good Financial Education for Youth Include?

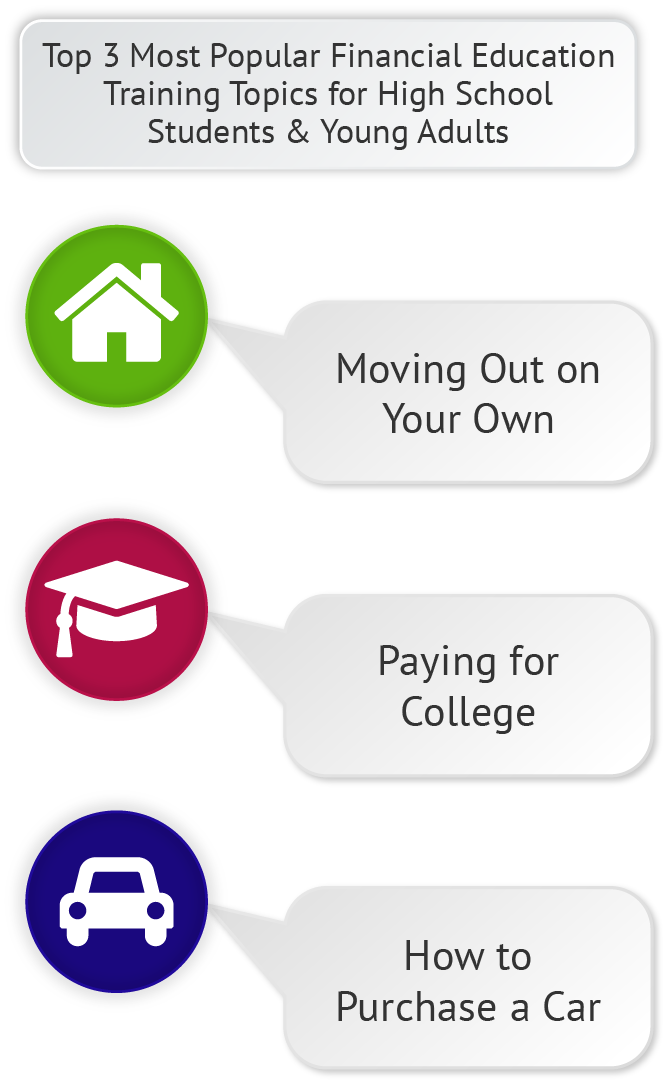

The best topics youth financial education should comprise are the ones that have immediate relevance in their lives. For example, many kids are transitioning toward moving out of their parents’ house and finding their own living spaces. Along with that transition comes the need to know how to set up a budget and smart financial goals, fill out a rental application, look responsible to a landlord, and prepare to meet all the expenses of renting an apartment.

Another relevant subject is how to purchase a truck or car. This life event is likely to occur around the age when kids are eligible to get their driver’s licenses. They might have dreams of getting a brand-new Porsche or Corvette, but financial education should guide them to choose a practical vehicle that fits with their budget and goals. Adolescents also need to learn how to apply for a car loan, what factors are considered in the qualification process, and how to buy insurance, so a youth money management course could cover those subjects too.

The third pertinent topic is how to pay for advanced education. If youth are bound for university, college, or trade school, they’ll need to understand all the expenses involved in their schooling. Career planning and return on investment of any educational path should be part of the instruction, as should the wide range of options for funding their chosen pursuit. It’s unlikely that they’ll be exposed to a personal finance course for college students, so the high school years are a good time to address these topics.

Knowing Kids’ Challenges Makes Youth Financial Education Better

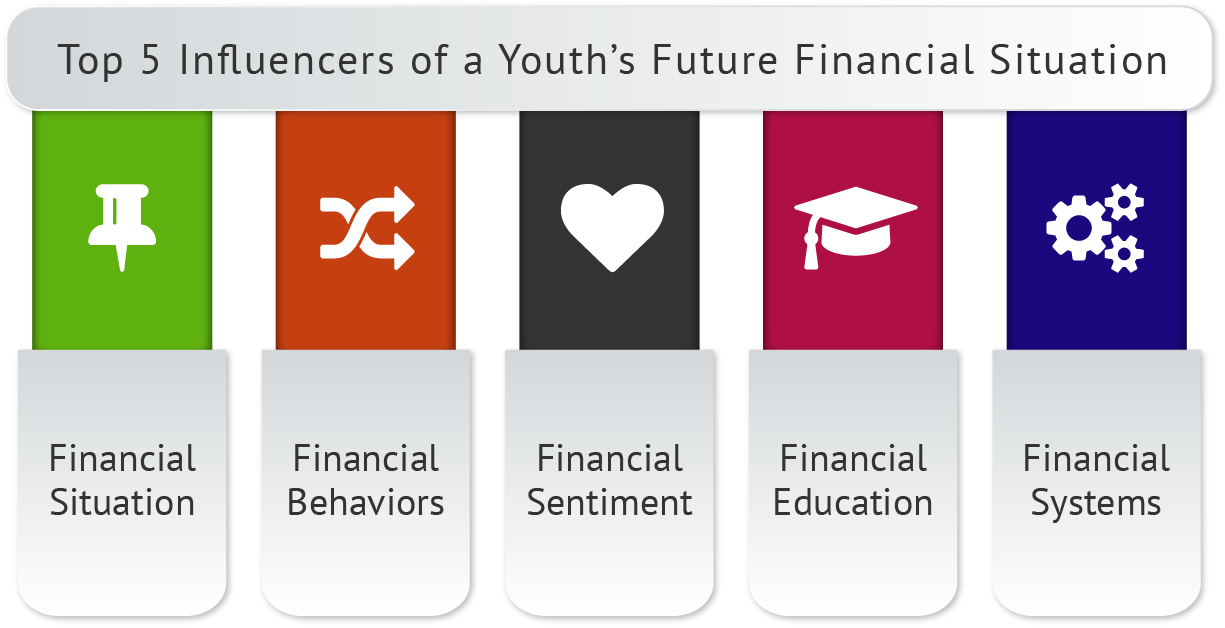

Youth financial education programs are scarce in today’s public school environment. When it comes to the production of self-reliant, independent young adults, schools and parents are failing to deliver. At the same time, teens are more and more able to get credit cards. So at the very moment when they lack important money management skills, they’re being faced with greater temptation to spend money they don’t actually have. There is also evidence that states with financial education requirements equip teens to make better decisions about how to pay for college.

A personal finance curriculum for high school kids should also address the financial behaviors they’ve already developed. Habits form young, and many kids are exposed to a broad scope of influences that lead them to form negative patterns of money handling. Advertising and peer pressure are two important ones; parents also exert influence on youth financial practices.

In terms of parent influences, simply the family into which a child is born makes a difference in their financial capabilities and knowledge. Kids see how their parents struggle with money decisions and pick up on their sentiments and attitudes toward personal finances. These attitudes can become ingrained as either positive or negative habits, depending on the family’s situation.

Kids also are graduating from secondary school without having learned how to set up the money management systems they need to get started in life. Raising youth financial capability should include teaching them how to systematize their accounting, for example, having checking, retirement, and savings accounts in place.

Youth Financial Education

You know how important it is for your kids to learn about money. But are you also aware that they are unlikely to receive any youth financial education in school? Public education systems are dealing with dwindling budgets, which means schools can scarcely afford to maintain the programs they have—much less add any. Therefore it’s up to you to provide your children with the financial skills they need to make it in today’s real-world economy.

The National Financial Educators Council (NFEC) promotes financial literacy for youth across the U.S. and around the globe. This organization is independent, not affiliated with corporate influences, and has adopted a social enterprise business model. The NFEC provides resources to parents to help them raise financially responsible children.

Most kids learn financial habits from their parents. But unfortunately, many parents received little or no financial education during their formative years. And parents who have made financial mistakes might not feel comfortable teaching their kids about money. According to Vince Shorb, young adult success coach at the NFEC, even those parents who have made errors in the past can find the resources to help teenagers become financially independent. After all, who hasn’t made at least one money misstep in his or her lifetime?

Financial education for youth has never been more important than it is today. And if they do receive a sound financial education, youth will have easier, more productive lives in the future. Financial knowledge gets passed along generation to generation. Children see how their parents handle money and pick up habits from watching them. But for parents, learning the basics of personal money management is easier and quicker than most subjects they studied in high school. Parents can—and should—start making a difference now.