Benefits of Financial Education in Schools

How does one begin to enumerate the benefits of financial education in schools? Financial education as part of a school’s curriculum is so vital to a successful life, it seems almost flippant to just make a list of the benefits. When financial literacy is taught in school, students learn this foundational skill at the critical time, as they are just beginning to manage their own money. This means they are interested and involved in learning how to deal with money in the best way possible. They actively use these newfound skills in their lives, and these behaviors toward money stay with them throughout their lives. Armed with money management skills, these young adults never let themselves become overrun by debt and they are always the master of money.

Learning Financial Education in School Offers Many Benefits

Why is providing a financial education important? There are numerous benefits of financial education in schools, such as introducing positive financial habits at an impressionable time, preparing students for the workforce or part-time work in college and endowing students with vital expertise that can guide their financial decisions throughout life. The benefits of financial education in schools, however, appear to fall on deaf ears of public policy makers. Today, only a handful of states require a high school course in economics and even fewer make teaching financial education topics mandatory.

Young Adult Pessimism and Loan Default Result from Lack of Financial Education

11.5% of 2014 college graduates have loans in default (Federal Student Aid Office of the US Dept of Education). https://www2.ed.gov/offices/OSFAP/defaultmanagement/cdr.html

Only 16% of Americans between ages 18-26 are very optimistic about their financial future (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

“The number one problem in today’s generation and economy is the lack of financial literacy.” – Alan Greenspan, former Chairman of the Federal Reserve

“I think people don’t understand compound interest because typically no one ever explains it to them and the level of financial literacy in the US is very low.” – James Surowiecki, journalist at The New Yorker and author of “The Financial Page” column

Schools Need to Design Quality Financial Education Programs

Schools Need to Design Quality Financial Education Programs

If we are considering diverting money that could have funded STEM programs towards building financial education programs within our schools, how can we be so sure that financial literacy is beneficial to our students? The public policy maker or concerned community citizen asking themselves this question can assuage their doubts by examining the academic literature that time and time again has proved the benefits of financial literacy. A reduction in the constitution of poor financial habits and the formation of better habits has been observed repeatedly.

The Coalition of Higher Education Assistance Organizations (COHEAO) conveyed that participants become more invested in learning when they can connect the skills they are being taught in class to some real-world usage in the short-term (Coalition of Higher Education Assistance Organizations). http://www.coheao.com/wp-content/uploads/2011/04/COHEAO-Whitepaper-Financial-Literacy-on-Campus-.pdf

The Canadian Task Force for Financial Literacy stressed that the program must have a framework in place to provide accountability and improve program outcomes. (Canadian Task Force for Financial Literacy). http://publications.gc.ca

“Financial literacy is just as important in life as the other basics.” – John W. Rogers, Jr., CEO Ariel Capital Management

Financial Education Courses in School are Life-Changing

Researchers asked individuals two sets of questions, one pertaining to basic financial literacy while the other related to advanced financial knowledge. The researchers then applied statistical techniques to construct indexes of financial knowledge. The probability of participating in the stock market increased 14 percentage points with a one standard deviation increase in advanced financial knowledge. In addition, a one standard deviation increase in basic financial literacy increases the probability of saving for retirement by 20 percentage points (De Nederlandsche Bank). https://www.dnb.nl/en/binaries/working%20paper%20313_tcm47-257145.pdf

One team of researchers decided to analyze the efficacy of simulations in producing behavioral change in students. Students who took Junior Achievement’s Finance park, a simulation for middle school students that sees students assume family and income scenarios, were split up into two groups after going through the park the first time. One group underwent financial education training while the other group did not. After 12 weeks, all the students went through the park for a second time. Over half the students in the group that received training were able to successfully construct a budget, a statistically significant amount over the only 1 student who was able to do so before the training (National Bureau of Economic Research). http://www.nber.org/papers/w16271.pdf

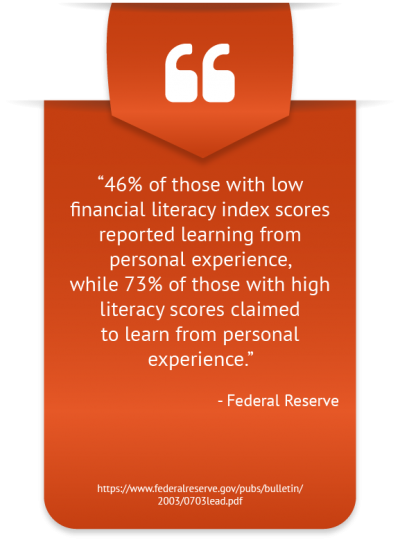

46% of those with low financial literacy index scores reported learning from personal experience, while 73% of those with high literacy scores claimed to learn from personal experience (Federal Reserve). https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

An additional year of schooling increases the probability of having an investment income by 4.4% for whites and 1.7% for blacks (Harvard Business School). http://www.people.hbs.edu/scole/webfiles/cole-shastry-smarts%20HBS%20working%20paper.pdf

Need for Financial Education in School is Evident in Adults

65% of adults in the United States report using a saving account (National Foundation for Credit Counseling). https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

15% of adults roll over $2,500 or more in credit card debt each month (National Foundation for Credit Counseling). https://www.nfcc.org/wp-content/uploads/2017/03/NFCC_BECU_2017-FLS_datasheet-with-key-findings.pdf

44% of Americans aged 22-26 do their own taxes (Bank of America). https://about.bankofamerica.com/assets/pdf/BOA_BMH_2016-REPORT-v5.pdf

Mandatory Financial Education

The many benefits of financial education in schools are, unfortunately, not realized by most public financial education certification directors who do not incorporate such vital courses into their school curriculum. If the benefits of financial education in school are to be realized, financial education companies and concerned individuals must advocate for a public financial education curriculum that, at a minimum, mandates a course in basic financial literacy to be completed in order to graduate.